The Indian banking sector’s asset quality improved during 2022-23 and 2023-24, with the gross non-performing assets (GNPA) ratio declining to its lowest in a decade. The combined balance sheet of scheduled commercial banks (SCBs) expanded at an accelerated pace, driven by credit to retail and services sectors, with higher net interest income and lower provisioning requirements boosting profitability. 1. Introduction IV.1 During 2022-23, the combined balance sheet of commercial banks expanded in double digits, driven by sustained credit growth. Lower slippages helped improve asset quality across all bank groups, with GNPA to total advances ratio of SCBs dropping to a 10-year low. Higher lending rates and lower provisioning requirements helped to improve the profitability of banks and shored up their capital positions. IV.2 Against this background, this chapter discusses the operations and performance of commercial banks during 2022-23 and H1:2023-24. An analysis of the consolidated balance sheet of SCBs is presented in Section 2, followed by an assessment of their financial performance in Section 3. The financial soundness of banks and the pattern of sectoral deployment of credit are discussed in Sections 4 and 5, respectively. Sections 6 and 7 deal with ownership patterns and corporate governance, respectively. Foreign banks’ operations in India and overseas operation of Indian banks are covered in Section 8, followed by developments in payments systems (Section 9) and consumer protection (Section 10) and financial inclusion (Section 11). Developments related to regional rural banks (RRBs), local area banks (LABs), small finance banks (SFBs) and payments banks (PBs) are examined in Sections 12 to 15. Section 16 concludes the chapter and offers a way forward. 2. Balance Sheet Analysis of SCBs IV.3 At end-March 2023, the Indian commercial banking space comprised 12 public sector banks (PSBs), 21 private sector banks (PVBs), 44 foreign banks (FBs), 12 SFBs, six PBs, 43 RRBs and two LABs. Of these 140 commercial banks, 136 were classified as scheduled while four banks were non-scheduled1. The consolidated balance sheet of SCBs (excluding RRBs) grew by 12.2 per cent in 2022-23, the highest in nine years. The main driver of this growth on the asset side was bank credit, which recorded its fastest pace of expansion in more than a decade (Chart IV.1 a). Deposit growth also picked up, although it trailed credit growth, resulting in higher recourse to borrowings (Chart IV.1b). This was particularly evident in the case of PSBs, for which the deposits to liabilities ratio moderated (Chart IV.1c).  IV.4 The share of PSBs in the consolidated balance sheet of SCBs declined from 58.6 per cent at end-March 2022 to 57.6 per cent at end-March 2023, while PVBs gained share from 34.0 per cent to 34.7 per cent. At end-March 2023, PSBs accounted for 61.4 per cent of total deposits of SCBs and 57.9 per cent of total advances (Table IV.1). 2.1 Liabilities IV.5 The aggregate deposits of SCBs picked up pace during 2022-23, led by term deposits of PVBs, benefitting from higher term deposit rates spurred by policy rate hikes during May 2022 – February 2023 and moderation of surplus liquidity (Chart IV.2). Interest rates on savings bank deposits — which account for around 31.4 per cent of total deposits — remained largely unchanged, which helped banks to post higher net interest margins (NIMs). | Table IV.1: Consolidated Balance Sheet of Scheduled Commercial Banks | | (At end-March) | | (Amount in ₹ crore) | | | Public Sector Banks | Private Sector Banks | Foreign Banks | Small Finance Banks # | Payments Banks | All SCBs | | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | | 1. Capital | 71,176 | 71,176 | 31,243 | 32,468 | 1,01,933 | 1,11,612 | 5,800 | 7,811 | 4,287 | 4,512 | 2,14,439 | 2,27,580 | | 2. Reserves and Surplus | 7,27,852 | 8,24,250 | 8,08,595 | 9,34,742 | 1,39,569 | 1,60,607 | 16,548 | 23,563 | (2,533) | (2,404) | 16,90,031 | 19,40,759 | | 3. Deposits | 1,07,17,362 | 1,17,09,581 | 54,64,241 | 62,99,332 | 8,45,482 | 8,55,825 | 1,45,731 | 1,91,372 | 7,829 | 12,174 | 1,71,80,645 | 1,90,68,284 | | 3.1. Demand Deposits | 7,23,258 | 7,48,951 | 7,84,134 | 8,85,497 | 2,78,677 | 2,89,545 | 5,767 | 7,456 | 30 | 393 | 17,91,866 | 19,31,842 | | 3.2. Savings Bank Deposits | 38,20,486 | 39,79,202 | 17,47,958 | 18,89,846 | 92,120 | 56,931 | 43,576 | 54,668 | 7,799 | 11,781 | 57,11,939 | 59,92,427 | | 3.3. Term Deposits | 61,73,618 | 69,81,428 | 29,32,149 | 35,23,990 | 4,74,685 | 5,09,349 | 96,388 | 1,29,248 | - | - | 96,76,840 | 1,11,44,014 | | 4. Borrowings | 7,51,301 | 9,03,824 | 7,57,261 | 8,12,969 | 1,27,467 | 2,08,739 | 27,011 | 31,171 | 307 | 519 | 16,63,348 | 19,57,222 | | 5. Other Liabilities and Provisions | 4,39,952 | 5,05,961 | 3,10,461 | 3,65,692 | 1,60,161 | 2,30,921 | 7,989 | 13,600 | 7,662 | 8,156 | 9,26,225 | 11,24,330 | | Total Liabilities/Assets | 1,27,07,643 | 1,40,14,793 | 73,71,801 | 84,45,203 | 13,74,612 | 15,67,704 | 2,03,080 | 2,67,517 | 17,552 | 22,957 | 2,16,74,688 | 2,43,18,174 | | | (58.6) | (57.6) | (34.0) | (34.7) | (6.3) | (6.4) | (0.9) | (1.1) | (0.1) | (0.1) | (100) | (100) | | 1. Cash and Balances with RBI | 7,68,668 | 6,41,731 | 5,76,127 | 4,13,201 | 1,44,544 | 93,411 | 16,414 | 17,840 | 1,529 | 2,295 | 15,07,282 | 11,68,479 | | 2. Balances with Banks and Money at Call and Short Notice | 4,96,434 | 4,23,343 | 1,60,149 | 2,36,221 | 1,16,468 | 1,19,332 | 2,531 | 4,538 | 3,228 | 4,963 | 7,78,810 | 7,88,397 | | 3. Investments | 35,95,647 | 38,17,201 | 16,26,884 | 18,75,137 | 5,05,001 | 6,74,077 | 41,661 | 58,062 | 9,937 | 12,064 | 57,79,131 | 64,36,540 | | 3.1 In Government Securities (a+b) | 29,93,865 | 32,22,899 | 13,68,853 | 15,87,677 | 4,68,711 | 6,31,129 | 36,683 | 52,137 | 9,924 | 12,049 | 48,78,036 | 55,05,891 | | a) In India | 29,50,409 | 31,65,076 | 13,51,118 | 15,73,022 | 3,98,009 | 5,88,166 | 36,683 | 52,137 | 9,924 | 12,049 | 47,46,144 | 53,90,449 | | b) Outside India | 43,456 | 57,824 | 17,735 | 14,655 | 70,702 | 42,963 | - | - | - | - | 1,31,892 | 1,15,442 | | 3.2 Other Approved Securities | 5 | 5 | - | - | - | - | - | - | - | - | 5 | 5 | | 3.3 Non-approved Securities | 6,01,777 | 5,94,296 | 2,58,031 | 2,87,460 | 36,290 | 42,948 | 4,978 | 5,925 | 13 | 15 | 9,01,090 | 9,30,644 | | 4. Loans and Advances | 70,43,940 | 82,83,763 | 45,53,541 | 53,66,675 | 4,65,484 | 4,91,029 | 1,35,802 | 1,77,887 | 2 | 0 | 1,21,98,769 | 1,43,19,355 | | 4.1 Bills Purchased and Discounted | 2,33,191 | 2,84,882 | 1,50,866 | 1,34,816 | 63,161 | 65,594 | 611 | 872 | - | - | 4,47,828 | 4,86,164 | | 4.2 Cash Credits, Overdrafts, etc. | 26,23,878 | 30,14,583 | 13,68,315 | 16,98,682 | 2,02,940 | 2,08,634 | 12,585 | 18,352 | - | - | 42,07,717 | 49,40,252 | | 4.3 Term Loans | 41,86,872 | 49,84,298 | 30,34,360 | 35,33,177 | 1,99,383 | 2,16,801 | 1,22,607 | 1,58,663 | 2 | 0 | 75,43,224 | 88,92,940 | | 5. Fixed Assets | 1,09,784 | 1,15,288 | 44,456 | 49,347 | 4,964 | 5,624 | 2,001 | 2,735 | 370 | 564 | 1,61,575 | 1,73,558 | | 6. Other Assets | 6,93,170 | 7,33,468 | 4,10,644 | 5,04,622 | 1,38,151 | 1,84,230 | 4,670 | 6,456 | 2,485 | 3,069 | 12,49,121 | 14,31,845 | Notes: 1. -: Nil/negligible.

2. #: Data pertain to 11 scheduled SFBs at end-March 2022 and 12 scheduled SFBs at end-March 2023.

3. Detailed bank-wise data on annual accounts are collated and published in Statistical Tables Relating to Banks in India, available at https://www.dbie.rbi.org.in.

4. Figures in parentheses are shares in total assets/liabilities of different bank groups in all SCBs.

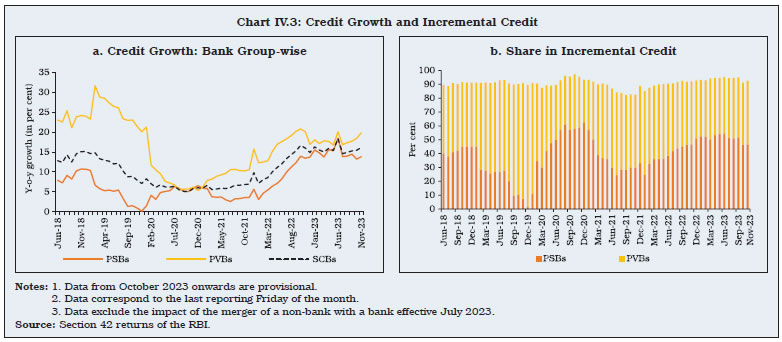

Source: Annual accounts of respective banks. | 2.2 Assets IV.6 Bank credit growth remained buoyant during 2022-23 and 2023-24. The year-on-year (y-o-y) credit growth at end-November 2023 was 16.2 per cent2 (Chart IV.3a). PSBs’ share in incremental credit increased during 2022-23 to reach 46.5 per cent at end-November 2023 (Chart IV.3b). IV.7 At end-March 2023, 81.2 per cent of SCBs’ investments were in government securities (G-secs) (Table IV.2). SLR investments of SCBs rose by 14.2 per cent in 2022-23 as compared with the growth of 9.0 per cent in the previous year, which pulled up the incremental investment-deposit (I-D) ratio (Chart IV.4). The held to maturity (HTM) limit of 23 per cent for SLR eligible securities was extended up to March 31, 2024 and banks were allowed to include securities acquired between September 1, 2020 and March 31, 2024 within the enhanced HTM limit3.

| Table IV.2: Investments of SCBs | | (At end-March) | | (Amount in ₹ crore) | | | PSBs | PVBs | FBs | SFBs | SCBs | | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | | Total Investments (A+B) | 36,03,007 | 38,33,030 | 16,32,570 | 18,81,756 | 4,77,085 | 6,55,830 | 41,695 | 58,244 | 57,54,358 | 64,28,860 | | A. SLR Investments (I+ II+III) | 27,87,114 | 30,07,757 | 13,40,152 | 15,62,365 | 4,06,226 | 5,99,061 | 36,711 | 52,151 | 45,70,203 | 52,21,335 | | I. Central Government Securities | 16,58,556 | 17,45,055 | 11,00,902 | 13,10,477 | 4,03,539 | 5,93,438 | 28,223 | 40,013 | 31,91,220 | 36,88,982 | | II. State Government Securities | 11,26,852 | 12,60,787 | 2,39,249 | 2,51,889 | 2,687 | 5,623 | 8,487 | 12,139 | 13,77,276 | 15,30,437 | | III. Other Approved Securities | 1,707 | 1,916 | - | - | - | - | - | - | 1,707 | 1,916 | | B. Non-SLR Investments (I+II) | 8,15,893 | 8,25,273 | 2,92,419 | 3,19,390 | 70,858 | 56,769 | 4,985 | 6,093 | 11,84,154 | 12,07,525 | | I. Debt Securities | 7,61,390 | 7,68,545 | 2,75,903 | 3,03,474 | 70,482 | 56,404 | 4,922 | 6,016 | 11,12,698 | 11,34,439 | | II. Equities | 54,503 | 56,728 | 16,515 | 15,916 | 376 | 365 | 62 | 77 | 71,456 | 73,087 | | Source: Off-site returns (global operations), RBI. | IV.8 The credit to deposit (C-D) ratio of banks increased from 74.9 per cent at end-November 2022 to 77.0 per cent at end-November 2023, on account of robust credit growth (Chart IV.4). 2.3 Maturity Profile of Assets and Liabilities IV.9 Mismatches in the maturity of assets and liabilities are intrinsic to the banking sector as deposits − their primary source of funds − have short- to medium-term maturities, while the repayment schedule of their loans typically stretches across the medium-term. As asset-liability mismatches expose them to interest rate risk and liquidity risk, careful monitoring and management assumes importance. During 2022-23, the maturity mismatch moderated in the short-term bucket4. The gap between assets and liabilities in the maturity bucket of over five years increased as banks took recourse to long-term borrowings (Chart IV.5). IV.10 All bank groups exhibited higher reliance on short-term borrowings relative to medium- to long-term borrowings, except SFBs. PVBs increased the share of their medium-and long-term borrowings during 2022-23. PSBs’ investments are typically in long-term instruments, while private sector counterparts prefer short-term exposures (Table IV.3). 2.4 International Liabilities and Assets IV.11 In 2022-23, international liabilities of Indian banks expanded in double digits on the back of 28.5 per cent y-o-y growth in the foreign currency non-resident (Bank) (FCNR(B)) deposits, reversing the fall of (-) 21.2 per cent in the previous year. With effect from July 07, 2022, the Reserve Bank temporarily withdrew the interest rate ceiling on incremental FCNR (B) deposits until October 31, 2022, which made FCNR(B) deposits relatively attractive. IV.12 Another factor which influenced the growth in international liabilities was a 20.0 per cent y-o-y growth in equities of banks held by non-residents, up from 8.7 per cent in the previous year. Based on the latest BIS guidelines, mark-to-market (MTM) derivatives have also been included in the international liabilities from September 2022, which constituted 3.4 per cent of their liabilities at end-March 2023 (Appendix Table IV.2). | Table IV.3: Bank Group-wise Maturity Profile of Select Liabilities/Assets | | (At end-March) | | (Per cent) | | Liabilities/Assets | PSBs | PVBs | FBs | SFBs | PBs | All SCBs | | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | | I. Deposits | | | | | | | | | | | | | | a) Up to 1 year | 35.0 | 36.4 | 32.3 | 33.0 | 62.8 | 65.8 | 50.2 | 42.2 | 11.8 | 15.5 | 35.6 | 36.7 | | b) Over 1 year and up to 3 years | 21.9 | 21.1 | 30.2 | 31.2 | 29.2 | 26.1 | 46.0 | 54.9 | 88.2 | 84.5 | 25.2 | 25.0 | | c) Over 3 years and up to 5 years | 12.7 | 12.8 | 9.7 | 9.1 | 8.0 | 8.1 | 1.6 | 1.8 | 0.0 | 0.0 | 11.4 | 11.2 | | d) Over 5 years | 30.5 | 29.7 | 27.8 | 26.7 | 0.0 | 0.0 | 2.2 | 1.1 | 0.0 | 0.0 | 27.9 | 27.1 | | II. Borrowings | | | | | | | | | | | | | | a) Up to 1 year | 54.3 | 62.2 | 50.0 | 45.9 | 80.5 | 90.5 | 37.1 | 38.8 | 100.0 | 100.0 | 54.1 | 58.1 | | b) Over 1 year and up to 3 years | 22.9 | 16.7 | 29.2 | 32.6 | 16.3 | 7.6 | 49.5 | 50.6 | 0.0 | 0.0 | 25.7 | 22.9 | | c) Over 3 years and up to 5 years | 14.0 | 8.5 | 11.5 | 10.3 | 1.6 | 0.7 | 9.2 | 5.4 | 0.0 | 0.0 | 11.8 | 8.3 | | d) Over 5 years | 8.8 | 12.6 | 9.3 | 11.2 | 1.6 | 1.2 | 4.2 | 5.2 | 0.0 | 0.0 | 8.4 | 10.7 | | III. Loans and Advances | | | | | | | | | | | | | | a) Up to 1 year | 25.2 | 28.3 | 30.4 | 28.4 | 53.3 | 56.1 | 38.2 | 36.5 | 100.0 | 100.0 | 28.3 | 29.4 | | b) Over 1 year and up to 3 years | 35.4 | 34.2 | 33.8 | 36.7 | 24.4 | 24.0 | 35.8 | 36.0 | 0.0 | 0.0 | 34.4 | 34.8 | | c) Over 3 years and up to 5 years | 15.1 | 14.1 | 13.4 | 12.5 | 10.3 | 10.0 | 11.1 | 10.5 | 0.0 | 0.0 | 14.2 | 13.3 | | d) Over 5 years | 24.4 | 23.4 | 22.3 | 22.4 | 12.1 | 9.9 | 14.9 | 17.1 | 0.0 | 0.0 | 23.0 | 22.5 | | IV. Investment | | | | | | | | | | | | | | a) Up to 1 year | 25.2 | 26.1 | 48.8 | 55.3 | 84.6 | 86.4 | 53.8 | 61.6 | 98.7 | 99.5 | 37.4 | 41.4 | | b) Over 1 year and up to 3 years | 16.4 | 14.7 | 22.4 | 19.1 | 10.3 | 8.2 | 25.6 | 27.0 | 0.8 | 0.1 | 17.6 | 15.4 | | c) Over 3 years and up to 5 years | 13.2 | 12.9 | 7.8 | 7.1 | 1.7 | 1.3 | 4.9 | 5.5 | 0.1 | 0.0 | 10.6 | 9.9 | | d) Over 5 years | 45.2 | 46.3 | 21.0 | 18.5 | 3.4 | 4.2 | 15.7 | 5.9 | 0.3 | 0.4 | 34.4 | 33.4 | Note: Figures denote share of each maturity bucket in each component of the balance sheet.

Source: Annual accounts of banks. | IV.13 On the other hand, international assets of banks in India contracted by 13.1 per cent in 2022-23 as compared with a growth of 9.0 per cent a year ago. The fall in assets in 2022-23 was on account of a reduction in overseas loans and holdings of international debt securities as banks deployed resources to fund domestic credit (Appendix Table IV.3). Consequently, the international assets to liabilities ratio of banks in India reduced at end-March 2023, after increasing for three consecutive years (Chart IV.6). IV.14 Banks’ consolidated international claims decelerated for all major economies, except Singapore (Appendix Table IV.4). At end-March 2023, their claims shifted away from banks towards non-financial private sectors (Chart IV.7a). The proportion of longer maturity claims increased, although short-term claims remained the dominant category (Appendix Table IV.5 and Chart IV.7b). 2.5 Off-Balance Sheet Operations IV.15 Contingent liabilities of SCBs grew by 22.4 per cent in 2022-23, led by growth in forward exchange contracts (Chart IV.8a). As a proportion to balance sheet size, contingent liabilities of SCBs increased from 132.8 per cent at end-March 2022 to 144.8 per cent at end-March 2023, with those of PSBs decreasing in 2022-23 to 36.5 per cent from 41.5 per cent in 2021-22 (Appendix Table IV.6). FBs’ contingent liabilities are more than 12 times their balance sheet size and constituted 55.3 per cent of the banking system’s total off-balance sheet (OBS) exposures (Chart IV.8b).

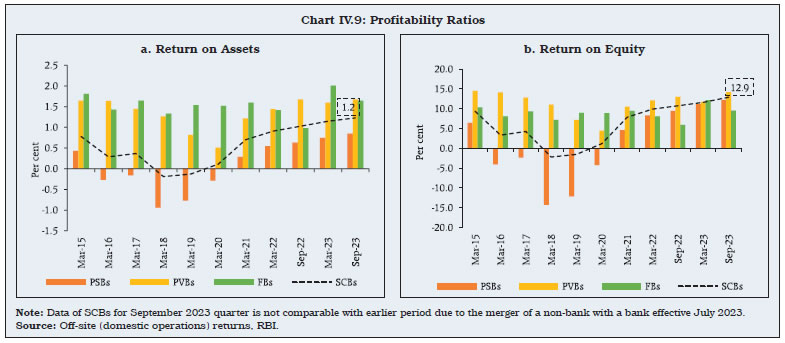

3. Financial Performance IV.16 The trend of improvement in the profitability of SCBs, which began in 2019-20, continued for the fourth consecutive year in 2022-23, aided by higher income and lower provisions and contingencies. Both return on assets (RoA) and return on equities (RoE) improved in 2022-23. (Chart IV.9). IV.17 Interest expended by SCBs had contracted for two consecutive years (2020-21 and 2021-22) reflecting the accommodative monetary policy stance. With a turn in the interest rate cycle, both interest income and interest outgo rose in 2022-23; as the expansion in interest income exceeded interest outgo, net interest income in 2022-23 was higher than in the previous year (Table IV.4).

| Table IV.4: Trends in Income and Expenditure of Scheduled Commercial Banks | | (Amount in ₹ crore) | | | Public Sector Banks | Private Sector Banks | Foreign Banks | Small Finance Banks # | Payments Banks | All SCBs | | 2021-22 | 2022-23 | 2021-22 | 2022-23 | 2021-22 | 2022-23 | 2021-22 | 2022-23 | 2021-22 | 2022-23 | 2021-22 | 2022-23 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | | 1. Income | 8,31,900 | 9,71,421 | 5,72,284 | 6,90,557 | 79,484 | 1,08,268 | 25,107 | 33,806 | 4,952 | 5,965 | 15,13,725 | 18,10,018 | | | (0.2) | (16.8) | (5.6) | (20.7) | (-1.1) | (36.2) | (12.0) | (34.6) | (393.2) | (20.5) | (2.5) | (19.6) | | a) Interest Income | 7,09,132 | 8,51,078 | 4,70,940 | 5,81,732 | 65,842 | 83,425 | 22,120 | 29,806 | 446 | 860 | 12,68,480 | 15,46,901 | | | (0.3) | (20.0) | (4.3) | (23.5) | (3.4) | (26.7) | (13.3) | (34.7) | (343.3) | (92.7) | (2.1) | (21.9) | | b) Other Income | 1,22,768 | 1,20,343 | 1,01,344 | 1,08,825 | 13,642 | 24,843 | 2,986 | 4,000 | 4,505 | 5,105 | 2,45,245 | 2,63,117 | | | (-0.3) | (-2.0) | (11.9) | (7.4) | (-18.2) | (82.1) | (3.2) | (34.0) | (398.7) | (13.3) | (4.7) | (7.3) | | 2. Expenditure | 7,65,360 | 8,66,772 | 4,76,060 | 5,66,421 | 61,099 | 78,123 | 24,133 | 29,644 | 5,041 | 5,844 | 13,31,693 | 15,46,804 | | | (-4.2) | (13.3) | (0.7) | (19.0) | (-0.5) | (27.9) | (18.4) | (22.8) | (286.6) | (15.9) | (-1.7) | (16.2) | | a) Interest Expended | 4,11,181 | 4,87,690 | 2,24,231 | 2,75,391 | 21,482 | 31,814 | 9,513 | 12,140 | 156 | 246 | 6,66,563 | 8,07,280 | | | (-4.7) | (18.6) | (-3.5) | (22.8) | (-0.4) | (48.1) | (4.3) | (27.6) | (181.4) | (57.5) | (-4.1) | (21.1) | | b) Operating Expenses | 2,20,091 | 2,44,064 | 1,56,614 | 2,02,616 | 24,972 | 27,958 | 9,813 | 13,152 | 4,882 | 5,579 | 4,16,372 | 4,93,369 | | | (8.0) | (10.9) | (20.1) | (29.4) | (11.8) | (12.0) | (30.0) | (34.0) | (290.3) | (14.3) | (13.9) | (18.5) | | of which: Wage Bill | 1,32,772 | 1,44,686 | 58,849 | 70,610 | 9,180 | 10,028 | 5,305 | 6,707 | 788 | 914 | 2,06,895 | 2,32,944 | | | (6.5) | (9.0) | (17.0) | (20.0) | (16.3) | (9.2) | (23.3) | (26.4) | (98.1) | (15.9) | (10.4) | (12.6) | | c) Provision and Contingencies | 1,34,088 | 1,35,018 | 95,216 | 88,415 | 14,645 | 18,351 | 4,807 | 4,352 | 3 | 20 | 2,48,758 | 2,46,155 | | | (-17.8) | (0.7) | (-13.2) | (-7.1) | (-16.3) | (25.3) | (29.6) | (-9.5) | (-228.9) | (556.9) | (-15.4) | (-1.1) | | 3. Operating Profit | 2,00,628 | 2,39,667 | 1,91,439 | 2,12,551 | 33,030 | 48,496 | 5,781 | 8,514 | (87) | 141 | 4,30,791 | 5,09,369 | | | (3.0) | (19.5) | (6.8) | (11.0) | (-9.4) | (46.8) | (0.6) | (47.3) | (-71.4) | (-263.0) | (3.6) | (18.2) | | 4. Net Profit | 66,540 | 1,04,649 | 96,223 | 1,24,136 | 18,385 | 30,145 | 974 | 4,162 | (90) | 121 | 1,82,032 | 2,63,214 | | | (109.1) | (57.3) | (38.5) | (29.0) | (-3.1) | (64.0) | (-52.2) | (327.6) | (-70.2) | (-235.6) | (49.2) | (44.6) | | 5. Net Interest Income (NII) | 2,97,950 | 3,63,388 | 2,46,708 | 3,06,341 | 44,360 | 51,611 | 12,608 | 17,666 | 290 | 615 | 6,01,917 | 7,39,621 | | | (8.1) | (22.0) | (12.6) | (24.2) | (5.3) | (16.3) | (21.2) | (40.1) | (541.7) | (111.7) | (10.0) | (22.9) | | 6. Net Interest Margin (NIM) (per cent) | 2.4 | 2.7 | 3.6 | 3.9 | 3.4 | 3.5 | 6.9 | 7.5 | 2.7 | 3.0 | 2.9 | 3.2 | Notes: 1. #: Data pertain to 11 scheduled SFBs at end-March 2022 and 12 scheduled SFBs at end-March 2023.

2. NIM has been defined as NII as percentage of average assets.

3. Figures in parentheses refer to per cent variation over the previous year.

Source: Annual accounts of respective banks. | IV.18 Supervisory data indicate that interest income from loans and advances grew by 24.0 per cent during 2022-23 and by 14.6 per cent from investments. On other hand, the interest expended rose by 18.1 per cent5. On balance, the NIM of banks increased by 36 bps to reach 3.8 per cent in 2022-23 (Chart IV.10). IV.19 During 2022-23, risk provisions of SCBs declined on account of lower slippages as also higher write-offs, upgradations and recoveries. This boosted banks’ net profits6, along with support from higher earnings (Chart IV.11a). Moreover, as asset quality improved, the provision coverage ratio (PCR) (without write-off adjusted) rose to 75.3 per cent by end-September 2023 (Chart IV.11b). IV.20 The spread between return on funds and cost of funds increased for SCBs. SFBs had wider spreads relative to other bank groups, reflecting relatively higher interest rates on advances (Table IV.5).

| Table IV.5: Cost of Funds and Return on Funds - Bank Group-wise | | (Per cent) | | Bank Group / Year | Cost of Deposits | Cost of Borrowings | Cost of Funds | Return on Advances | Return on Investments | Return on Funds | Spread (Column 8 – Column 5) | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | PSBs | 2021-22 | 3.7 | 4.2 | 3.7 | 6.9 | 6.1 | 6.6 | 2.9 | | | 2022-23 | 3.9 | 6.2 | 4.1 | 7.6 | 6.3 | 7.2 | 3.1 | | PVBs | 2021-22 | 3.7 | 5.2 | 3.9 | 8.5 | 5.8 | 7.7 | 3.9 | | | 2022-23 | 3.8 | 6.4 | 4.1 | 9.2 | 6.3 | 8.4 | 4.3 | | FBs | 2021-22 | 2.1 | 3.6 | 2.3 | 7.0 | 5.7 | 6.3 | 4.0 | | | 2022-23 | 2.9 | 4.1 | 3.1 | 8.2 | 5.8 | 6.9 | 3.7 | | SFBs | 2021-22 | 5.9 | 7.1 | 6.1 | 15.9 | 5.9 | 13.6 | 7.5 | | | 2022-23 | 5.9 | 7.3 | 6.1 | 16.5 | 6.7 | 14.2 | 8.0 | | PBs | 2021-22 | 2.9 | 2.8 | 2.9 | 5.2 | 5.1 | 5.1 | 2.2 | | | 2022-23 | 2.1 | 7.8 | 2.4 | 6.0 | 5.6 | 5.6 | 3.3 | | All SCBs | 2021-22 | 3.6 | 4.6 | 3.7 | 7.6 | 6.0 | 7.0 | 3.3 | | | 2022-23 | 3.8 | 6.1 | 4.0 | 8.3 | 6.3 | 7.7 | 3.6 | Notes: 1. Cost of deposits = Interest paid on deposits/Average of current and previous year’s deposits.

2. Cost of borrowings = (Interest expended - Interest on deposits)/Average of current and previous year’s borrowings.

3. Cost of funds = Interest expended / (Average of current and previous year’s deposits plus borrowings)

4. Return on advances = Interest earned on advances /Average of current and previous year’s advances.

5. Return on investments = Interest earned on investments /Average of current and previous year’s investments.

6. Return on funds = (Interest earned on advances + Interest earned on investments) / (Average of current and previous year’s advances plus investments).

Source: Calculated from balance sheets of respective banks. | 4. Soundness Indicators IV.21 During 2022-23, SCBs strengthened their capital buffers, improved asset quality and maintained sufficient liquid assets. At end-March 2023, there was no bank under the prompt corrective action (PCA) framework as compared to one at end-March 2022. 4.1 Capital Adequacy IV.22 The capital to risk-weighted assets ratio (CRAR) as well as Tier I capital ratio of SCBs has been rising gradually over time. Although all bank groups remained well-capitalised, the CRAR of PVBs declined marginally due to a higher increase in their risk-weighted assets (RWAs) vis-à-vis their capital funds (Table IV.6). Supervisory data indicate that the CRAR of SCBs reached 16.8 per cent at end-September 2023. | Table IV.6: Component-wise Capital Adequacy of SCBs | | (At end-March) | | (Amount in ₹ crore) | | | PSBs | PVBs | FBs | SCBs | | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | 1. Capital Funds | 8,67,386 | 10,16,789 | 8,80,664 | 10,20,953 | 2,19,852 | 2,43,109 | 19,93,133 | 23,13,517 | | i) Tier I Capital | 7,12,071 | 8,47,783 | 8,06,269 | 9,11,271 | 2,01,206 | 2,20,750 | 17,41,694 | 20,08,618 | | ii) Tier II Capital | 1,55,315 | 1,69,006 | 74,395 | 1,09,681 | 18,647 | 22,359 | 2,51,440 | 3,04,899 | | 2. Risk Weighted Assets | 59,32,875 | 65,48,771 | 46,90,393 | 54,85,172 | 11,09,550 | 12,26,073 | 1,18,43,786 | 1,34,00,008 | | 3. CRAR (1 as % of 2) | 14.6 | 15.5 | 18.8 | 18.6 | 19.8 | 19.8 | 16.8 | 17.3 | | Of which: Tier I | 12 | 13 | 17.2 | 16.6 | 18.1 | 18 | 14.7 | 15.0 | | Tier II | 2.6 | 2.6 | 1.6 | 2 | 1.7 | 1.8 | 2.1 | 2.3 | | Source: Off-site returns, RBI. |

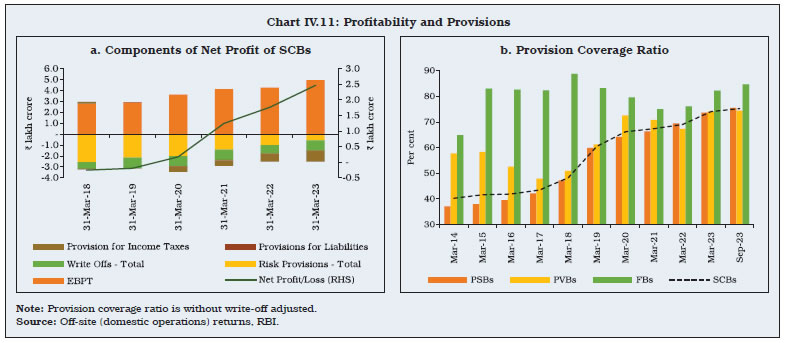

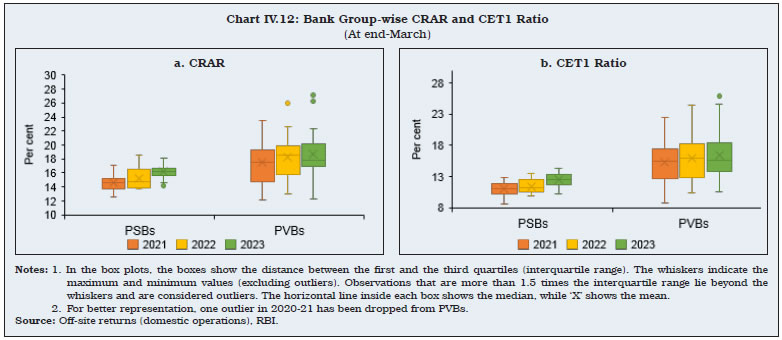

IV.23 At end-March 2023, all bank groups met the regulatory requirement of CRAR and common equity tier 1 (CET1) ratio. Although the divergence in capital positions of banks narrowed for bank groups, PVBs continued to have higher dispersion than PSBs. The first quartiles of PVBs’ CRAR and CET1 ratios were higher than PSBs’ third quartiles, mirroring stronger capital buffers of the former (Chart IV.12 a and b). IV.24 The resources raised by banks through private placements of debt, qualified institutional placements and preferential allotments of equity accelerated for the second consecutive year during 2022-23. Although the number of issues by PSBs declined during 2022-23, the total amount raised increased (Table IV.7). | Table IV.7: Resources Raised by Banks | | (Amount in ₹ crore) | | | 2020-21 | 2021-22 | 2022-23 | 2023-24 (Up to October) | | No. of issues | Amount raised | No. of issues | Amount raised | No. of issues | Amount raised | No. of issues | Amount raised | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | PSBs | 37 | 59,528 | 33 | 69,069 | 27 | 70,260 | 11 | 44,206 | | PVBs | 9 | 41,232 | 17 | 41,684 | 14 | 52,903 | 7 | 16,590 | | Foreign Banks | - | - | - | - | 2 | 224 | - | - | | Total | 46 | 1,00,760 | 50 | 1,10,753 | 43 | 1,23,387 | 18 | 60,796 | Notes: 1. Includes private placement of debt, qualified institutional placement and preferential allotment.

2. Data for 2023-24 are provisional.

Source: SEBI, BSE and NSE. |

| Table IV.8: Leverage Ratio and Liquidity Coverage Ratio | | (in per cent) | | | Leverage Ratio | Liquidity Coverage Ratio | | Mar-21 | Mar-22 | Mar-23 | Sep-23 | Mar-21 | Mar-22 | Mar-23 | Sep-23 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | PSBs | 5.0 | 5.1 | 5.6 | 5.5 | 169.8 | 155.8 | 153.5 | 141.3 | | PVBs | 9.7 | 9.7 | 9.6 | 9.5 | 136.1 | 127.7 | 127.9 | 122.9 | | FBs | 10.7 | 11.0 | 10.8 | 10.3 | 178.8 | 171.0 | 154.6 | 144.9 | | All SCBs | 7.0 | 7.2 | 7.4 | 7.4 | 158.9 | 147.1 | 144.6 | 135.4 | | Source: Off-site returns (global operations), RBI. | 4.2 Leverage and Liquidity IV.25 The leverage ratio (LR) — Tier 1 capital as a proportion of total exposures — is a non-risk based backstop measure which complements the Basel III risk-based capital framework. Domestic systemically important banks (D-SIBs) in India are required to maintain it at 4 per cent and other banks at 3.5 per cent vis-à-vis the Basel III recommendation of 3 per cent. At end-March 2023, all bank groups met the minimum requirement (Table IV.8). IV.26 The liquidity coverage ratio (LCR) is designed to ensure that banks hold a sufficient reserve of high-quality liquid assets (HQLAs) to enable them to survive a period of significant liquidity stress lasting 30 calendar days. At end-March 2023, all bank groups held significantly higher HQLAs than the stipulated requirement of 100 per cent of 30 days’ net cash outflows (Table IV.8). IV.27 The net stable funding ratio (NSFR) – the ratio of available stable funding to the required stable funding – limits overreliance of banks on short-term wholesale funding, encourages better assessment of funding risk across all on- and off-balance sheet items, and promotes funding stability. In line with international standards, banks in India are required to maintain NSFR at a minimum of 100 per cent. At end-March 2023, all bank groups met this target (Table IV.9). 4.3 Non-Performing Assets IV.28 The improvement in asset quality of banks, measured by their GNPA ratios, that began in 2018-19 continued during 2022-23. The GNPA ratio of SCBs fell to a decadal low of 3.9 per cent at end-March 2023 and further to 3.2 per cent at end-September 2023. During 2022-23, around 45 per cent of reduction in GNPAs of SCBs was contributed by recoveries and upgradations (Table IV.10). | Table IV.9: Net Stable Funding Ratio | | (At end-March 2023) | | (Amount in ₹ crore) | | | Available Stable Funding | Required Stable Funding | NSFR (per cent) | | 1 | 2 | 3 | 4 | | Public Sector Banks | 1,05,60,943 | 81,99,214 | 128.8 | | Private Sector Banks | 61,38,281 | 47,68,581 | 128.7 | | Foreign Banks | 6,54,059 | 5,12,992 | 127.5 | | Small Finance Banks | 1,96,403 | 1,49,046 | 131.8 | | Scheduled Commercial Banks | 1,75,49,686 | 1,36,29,833 | 128.8 | | Source: Off-site returns, RBI. |

| Table IV.10: Movements in Non-Performing Assets by Bank Group | | (Amount in ₹ crore) | | | PSBs | PVBs | FBs | SFBs# | All SCBs | | 1 | 2 | 3 | 4 | 5 | 6 | | Gross NPAs | | | | | | | Closing Balance for 2021-22 | 5,42,174 | 1,80,769 | 13,786 | 6,911 | 7,43,640 | | Opening Balance for 2022-23 | 5,42,174 | 1,80,769 | 13,786 | 10,684 | 7,47,413 | | Addition during the year 2022-23 | 98,291 | 1,10,064 | 5,971 | 6,901 | 2,21,228 | | Reduction during the year 2022-23 | 2,12,268 | 1,65,619 | 10,231 | 8,977 | 3,97,095 | | i. Recovered | 61,195 | 40,447 | 5,844 | 2,368 | 1,09,853 | | ii. Upgradations | 23,084 | 41,225 | 3,102 | 2,639 | 70,049 | | iii. Written-off | 1,27,990 | 83,947 | 1,286 | 3,970 | 2,17,193 | | Closing Balance for 2022-23 | 4,28,197 | 1,25,214 | 9,526 | 8,608 | 5,71,546 | | Gross NPAs as per cent of Gross Advances* | | | | | | | Closing Balance for 2021-22 | 7.3 | 3.8 | 2.9 | 4.9 | 5.8 | | Closing Balance for 2022-23 | 5.0 | 2.3 | 1.9 | 4.7 | 3.9 | | Net NPAs | | | | | | | Closing Balance for 2021-22 | 1,54,745 | 43,738 | 3,023 | 2,725 | 2,04,231 | | Closing Balance for 2022-23 | 1,02,532 | 29,507 | 1,672 | 1,622 | 1,35,333 | | Net NPAs as per cent of Net Advances | | | | | | | 2021-22 | 2.2 | 1.0 | 0.6 | 2.0 | 1.7 | | 2022-23 | 1.2 | 0.5 | 0.3 | 0.9 | 0.9 | Notes: 1. #: Data include scheduled SFBs.

2. *: Calculated by taking gross NPAs from annual accounts of respective banks and gross advances from off-site returns (global operations).

3. The difference in the closing balance for 2021-22 and opening balance for 2022-23 in GNPAs for SFBs is due to the inclusion of a new SFB in the second schedule of the Reserve Bank of India Act, 1934 on July 06, 2022 with an opening balance for 2022-23.

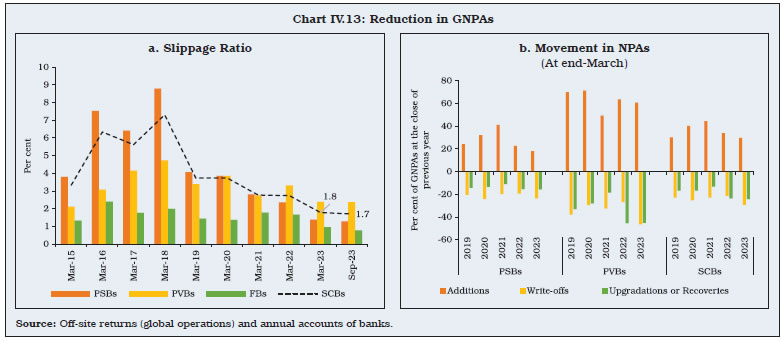

Source: Annual accounts of banks and off-site returns (global operations), RBI. | IV.29 The slippage ratio — which measures new accretions to NPAs as a share of standard advances at the beginning of the year — moderated during 2022-23 and further in H1:2023-24 (Chart IV.13a). A mix of write-offs, upgradations and recoveries contributed to reduction in NPAs (Chart IV.13b).

| Table IV.11: Classification of Loan Assets by Bank Group | | (Amount in ₹ crore) | | Bank Group | End-March | Standard Assets | Sub-Standard Assets | Doubtful Assets | Loss Assets | | Amount | Per cent* | Amount | Per cent* | Amount | Per cent* | Amount | Per cent* | | PSBs | 2022 | 61,96,644 | 92.4 | 75,855 | 1.1 | 3,29,369 | 4.9 | 1,02,403 | 1.5 | | | 2023 | 72,86,427 | 94.8 | 62,444 | 0.8 | 2,28,806 | 3.0 | 1,10,054 | 1.4 | | PVBs | 2022 | 43,63,690 | 96.3 | 41,251 | 0.9 | 77,394 | 1.7 | 50,619 | 1.1 | | | 2023 | 51,99,732 | 97.8 | 34,288 | 0.6 | 52,469 | 1.0 | 29,033 | 0.5 | | FBs | 2022 | 4,62,299 | 97.1 | 3,649 | 0.8 | 7,953 | 1.7 | 2,184 | 0.5 | | | 2023 | 4,89,212 | 98.1 | 1,697 | 0.3 | 6,648 | 1.3 | 1,182 | 0.2 | | SFBs** | 2022 | 1,33,092 | 95.1 | 5,039 | 3.6 | 1,833 | 1.3 | 39 | 0.0 | | | 2023 | 1,76,199 | 95.3 | 3,035 | 1.6 | 2,491 | 1.3 | 3,082 | 1.7 | | All SCBs | 2022 | 1,11,55,725 | 94.1 | 1,25,793 | 1.1 | 4,16,550 | 3.5 | 1,55,245 | 1.3 | | | 2023 | 1,31,51,571 | 96.1 | 1,01,465 | 0.7 | 2,90,414 | 2.1 | 1,43,351 | 1.0 | Notes: 1. *: As per cent of gross advances.

2. **: Refers to scheduled SFBs.

Source: Off-site returns (domestic operations), RBI. | IV.30 The increase in the proportion of standard assets to total advances was sustained for all bank groups during 2022-23. The amount of NPAs decreased for all bank groups, except SFBs (Table IV.11). IV.31 The share of large borrowal accounts (accounts with total exposure of ₹5 crore and above) in total advances declined to 46.4 per cent at end-March 2023 from 47.8 per cent a year ago. Their contribution to total NPAs also fell during the year to 53.9 per cent from 64.0 per cent. The SMA-1 and SMA-2 ratios, which indicate potential stress, declined across bank groups for overall as well as large borrowal accounts (Chart IV.14). IV.32 In retrospect, the pandemic’s impact was less than initially feared for larger and industrial sector firms. Moreover, the impact across firms and sectors was transient (Box IV.1).

Box IV.1: COVID-19 Scarring Impact on Borrowers Borrower default probabilities are influenced by firm-specific characteristics, such as leverage, profitability, liquidity, recent sales performance, investment policy as well as default history (Bonfim, 2008 and Fukuda et al., 2008). A major macroeconomic shock such as COVID-19 with large output losses and disruptions can have a sizeable impact on loan repayments. Bank-borrower-level data available in Central Repository of Information on Large Credits (CRILC) were matched with firm-level data on a quarterly basis for the period June 2018 to March 20227. Using this bank-firm-time level database, the following panel fixed effects linear probability model was estimated:  where the dependent variable (Yibt) is a dummy variable taking the value of 1 in case of an asset classification downgrade, i.e., if a firm i’s loan from bank b in quarter t is downgraded, and 0 otherwise. Thus, any downward transition in period t from t-1, including from standard to special mention accounts, is considered a downgrade. Covidt is a dummy variable which takes the value of 1 in the post-pandemic period, i.e., March 2020 onwards, and 0 otherwise. FirmCharit represents firm characteristics, viz., its sector8 and size (log of total assets), which are used alternately in the regression. ACSt, representing the asset classification standstill, takes the value of 1 for March 2020 and June 20209. Xit represents other firm-level controls, including profitability (profit-after-tax to income ratio), liquidity (current ratio) and leverage (debt to assets ratio). The empirical analysis suggests that the likelihood of downgrade of a typical firm was muted during the asset classification standstill period, but it edged up after the dispensation was withdrawn. The baseline specification suggests that larger, more profitable, highly liquid and less leveraged firms had lower likelihood of downgrades (Model 1). Interacting the COVID-19 dummy with firm specific characteristics reveals that larger firms could sustain the negative impact of the pandemic better and had a relatively lower likelihood of downgrades in the post-pandemic period (Model 2). Industrial sector firms had relatively lower likelihood of downgrades post-COVID, as compared with firms in the services sector, reflecting the outsize impact of the pandemic on services relative to industrial sector (Model 3). | Table IV.1.1: Regression Results | | | Dependent variable (Y) = downgrade likelihood | | (1) | (2) | (3) | | COVID | 0.0103*** | 0.0202*** | 0.0160*** | | | (0.0028) | (0.0074) | (0.0031) | | ACS | -0.0180*** | -0.0182*** | -0.0181*** | | | (0.0048) | (0.0049) | (0.0049) | | PAT-income ratio | -0.0132*** | -0.0132*** | -0.0136*** | | | (0.0018) | (0.0018) | (0.0018) | | Current Ratio | -0.0024*** | -0.0025*** | -0.0019** | | | (0.0008) | (0.0008) | (0.0007) | | Debt-Asset Ratio | 0.0553*** | 0.0552*** | 0.0530*** | | | (0.0070) | (0.0069) | (0.0070) | | Log Assets | -0.0093*** | -0.0086*** | -0.0091*** | | | (0.0024) | (0.0025) | (0.0025) | | COVID*Log Assets | | -0.0011* | | | | | (0.0006) | | | COVID*Sector | | | -0.0075*** | | | | | (0.0017) | | Constant | 0.1010*** | 0.0946*** | 0.0987*** | | | (0.0215) | (0.0225) | (0.0215) | | Firm Fixed Effects | Yes | Yes | Yes | | Observations | 396,984 | 396,984 | 388,923 | | R-squared | 0.129 | 0.129 | 0.129 | Robust standard errors in parentheses

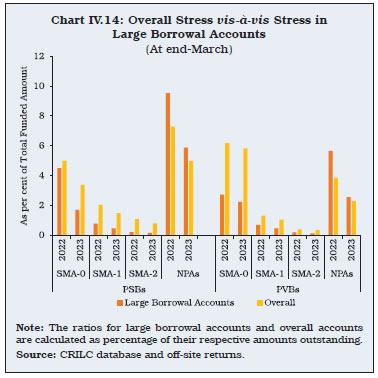

*** p<0.01, ** p<0.05, * p<0.1

Note: Standard errors are clustered at the bank level and adjusted for heteroscedasticity. | To sum up, although the likelihood of downgrades increased in the immediate aftermath of COVID-19, the impact was relatively less on larger firms and industrial sector firms. Thus, the pandemic’s scarring was transitory, facilitated by proactive monetary, regulatory and fiscal support. References Bonfim, D. (2008), “Credit Risk Drivers: Evaluating the Contribution of Firm Level Information and of Macroeconomic Dynamics”, Journal of Banking and Finance, 33(2): 281-299. Fukuda, S., Kasuya, M. and Akashi, K. (2008), “Impaired Bank Health and Default Risk”, Pacific-Basin Finance Journal, 17(2):145-162. | IV.33 Following the Reserve Bank’s resolution frameworks 1.0 and 2.0 announced in response to COVID-19 related disruptions, the number of restructured accounts peaked in 2021-22. With this special dispensation coming to an end, they moderated in 2022-23 (Chart IV.15a). The share of restructured standard advances (RSA) in gross loans and advances decreased from 1.8 per cent at end-March 2022 to 1.2 per cent at end-March 2023, led by PVBs (Chart IV.15b). 4.4 Recoveries IV.34 Amongst the multiple channels through which banks resolve their stressed assets, debt recovery tribunals (DRTs) witnessed the highest growth rate in the number of referred cases as also the amount involved during 2022-23. After a sharp increase in the previous year, referred cases as well as amount involved contracted for cases under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act. The Insolvency and Bankruptcy Code (IBC) remained the dominant mode of recovery, with a share of 43.0 per cent in the total amount recovered in 2022-23 and the recovery rate also improved (Table IV.12). IV.35 Apart from recovery through various resolution mechanisms, banks also clean up their balance sheets through sale of NPAs to asset reconstruction companies (ARCs). Sales to ARCs shot up in 2022-23, partly reflecting assets sold to the newly operationalised National Assets Reconstruction Company Ltd (NARCL). During 2022-23, 9.7 per cent of the previous year’s stock of SCBs’ GNPAs was sold to ARCs as compared with only 3.2 per cent in 2021-22 (Chart IV.16a). On the other hand, the acquisition cost of ARCs as a proportion to book values of assets declined from 33 per cent at end-March 2022 to 29.8 per cent at end-March 2023 (Chart IV.16b). | Table IV.12: NPAs of SCBs Recovered through Various Channels | | (Amount in ₹ crore) | | Recovery Channel | 2021-22 | 2022-23 (P) | | No. of cases referred | Amount involved | Amount recovered* | Col. (4) as per cent of Col. (3) | No. of cases referred | Amount involved | Amount recovered* | Col. (8) as per cent of Col. (7) | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | Lok Adalats | 85,06,741 | 1,19,006 | 2,778 | 2.3 | 1,42,49,462 | 1,88,527 | 3,831 | 2.0 | | DRTs | 30,651 | 68,956 | 12,035 | 17.5 | 58,073 | 4,02,636 | 36,924 | 9.2 | | SARFAESI Act | 2,49,645 | 1,21,718 | 27,349 | 22.5 | 1,85,397 | 1,11,805 | 30,864 | 27.6 | | IBC @# | 891 | 1,97,959 | 47,409 | 23.9 | 1,261 | 1,33,930 | 53,968 | 40.3 | | Total | 87,87,928 | 5,07,639 | 89,571 | 17.6 | 1,44,94,193 | 8,36,898 | 1,25,587 | 15.0 | Notes: 1. P: Provisional.

2. *: Refers to the amount recovered during the given year, which could be with reference to the cases referred during the given year as well as during the earlier years.

3. @: Data in columns 2 and 6 are the cases admitted by National Company Law Tribunals (NCLTs) under IBC.

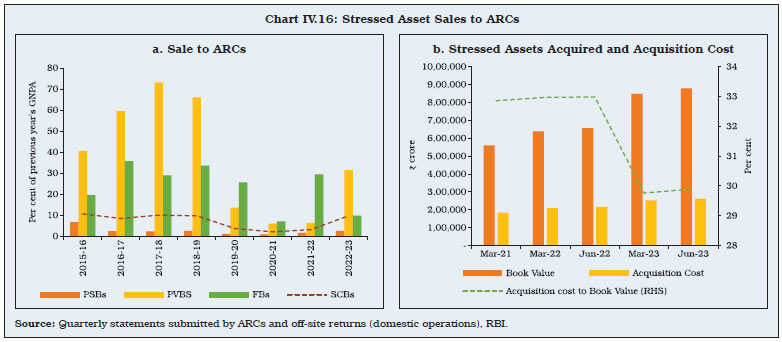

4. #: Data in columns 3 to 5 and 7 to 9 pertain to financial creditors. It covers 147 and 184 resolution plans approved during 2021-22 and 2022-23, respectively.

Source: Off-site returns, RBI and Insolvency and Bankruptcy Board of India (IBBI). |

IV.36 The share of SRs subscribed by banks and FIs has steadily declined from 65.4 per cent at end-March 2021 to 60.6 per cent at end-March 2023. The amount of SRs completely redeemed, an indicator of recovery through this mode, increased further during the year (Table IV.13). 4.5 Frauds in the Banking Sector IV.37 Frauds lead to reputational, operational and business risk for banks and undermine customers’ trust in the banking system with financial stability implications. During 2022-23, the total amount of frauds reported by banks declined to a six-year low while the average amount involved in frauds was the lowest in a decade (Appendix Table IV.7). In H1:2023-24, although the number of frauds reported rose over the corresponding period a year ago, the amount involved was only 14.9 per cent of the previous year’s amount (Table IV.14). | Table IV.13: Details of Financial Assets Securitised by ARCs | | (At end-March) | | (Amount in ₹ crore) | | | 2021 | 2022 | 2023 | | 1 | 2 | 3 | 4 | | Number of reporting ARCs | 28 | 29 | 28 | | 1. Book Value of Assets Acquired | 5,60,492 | 6,38,008 | 8,48,119 | | 2. Security Receipt Issued by SCs/ RCs | 1,79,560 | 2,04,844 | 2,46,290 | | 3. Security Receipts Subscribed to by | | | | | (a) Selling Banks/FIs | 1,17,551 | 1,28,007 | 1,49,253 | | (b) SCs/RCs | 35,522 | 41,353 | 49,519 | | (c) FIIs | 11,427 | 15,069 | 19,383 | | (d) Others (Qualified Institutional Buyers) | 15,060 | 20,415 | 28,135 | | 4. Amount of Security Receipts Completely Redeemed | 25,223 | 31,331 | 41,058 | | 5. Security Receipts Outstanding | 1,19,413 | 1,25,373 | 1,39,423 | Note: 1. Total as at the end of quarter (Cumulative/stock figures).

2. SCs- Securitisation Companies and RCs – Reconstruction Companies.

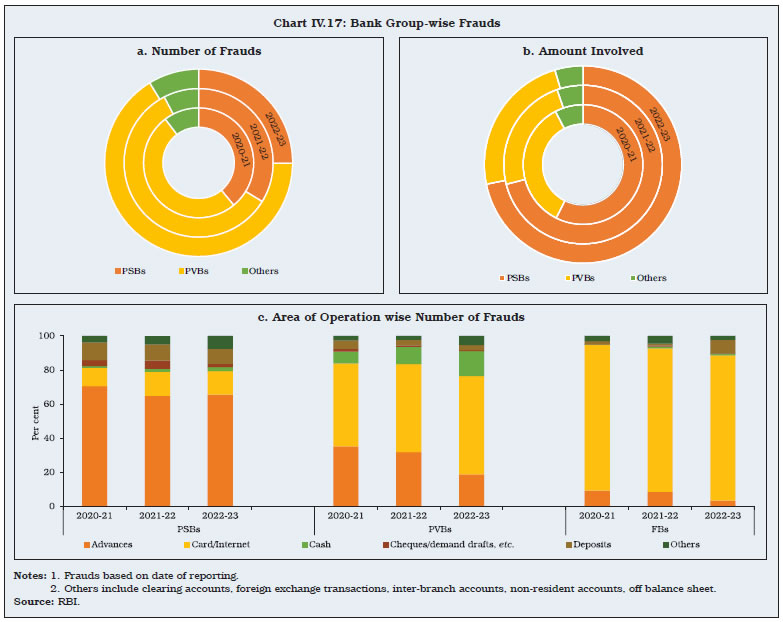

Source: Quarterly statements submitted by ARCs. |

| Table IV.14: Frauds in Various Banking Operations Based on the Date of Reporting | | (Amount in ₹ crore) | | Area of Operation | 2020-21 | 2021-22 | 2022-23 | 2022-23 (April-Sep) | 2023-24 (April-Sep) | | Number of frauds | Amount involved | Number of frauds | Amount involved | Number of frauds | Amount involved | Number of frauds | Amount involved | Number of frauds | Amount involved | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | | Advances | 3,401 | 1,17,018 | 3,789 | 43,512 | 4,101 | 25,177 | 1,998 | 16,968 | 1,139 | 1,765 | | Off-balance Sheet | 23 | 535 | 21 | 1,077 | 15 | 298 | 5 | 283 | 4 | 73 | | Forex Transactions | 4 | 129 | 7 | 7 | 13 | 12 | 10 | 3 | 5 | 5 | | Card/Internet | 2,545 | 119 | 3,596 | 155 | 6,699 | 277 | 2,321 | 87 | 12,069 | 630 | | Deposits | 504 | 434 | 471 | 493 | 652 | 258 | 270 | 135 | 915 | 103 | | Inter-Branch Accounts | 2 | 0 | 3 | 2 | 3 | 0 | 2 | 0 | 0 | 0 | | Cash | 329 | 39 | 649 | 93 | 1,485 | 159 | 589 | 81 | 210 | 31 | | Cheques/DDs, etc. | 163 | 85 | 201 | 158 | 118 | 25 | 73 | 12 | 60 | 14 | | Clearing Accounts, etc. | 14 | 4 | 16 | 1 | 18 | 3 | 11 | 2 | 2 | 0 | | Others | 278 | 54 | 300 | 100 | 472 | 423 | 117 | 114 | 79 | 21 | | Total | 7,263 | 1,18,417 | 9,053 | 45,598 | 13,576 | 26,632 | 5,396 | 17,685 | 14,483 | 2,642 | Notes: 1. Refers to frauds of ₹1 lakh and above.

2. The figures reported by banks and financial institutions are subject to change based on revisions filed by them.

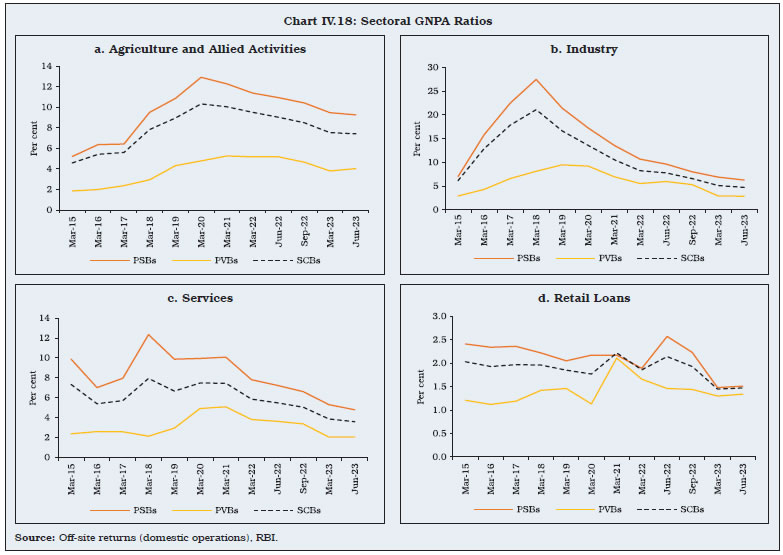

3. Frauds reported in a year could have occurred several years prior to year of reporting.

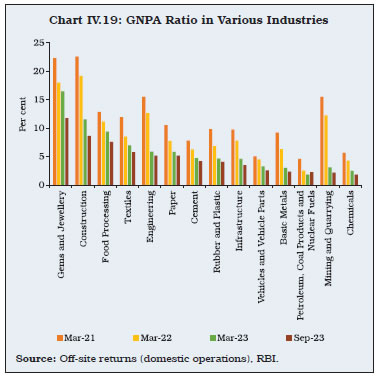

4. Amounts involved are as reported and do not reflect the amount of loss incurred. Depending on recoveries, the loss incurred gets reduced. Further, the entire amount involved in loan accounts is not necessarily diverted.

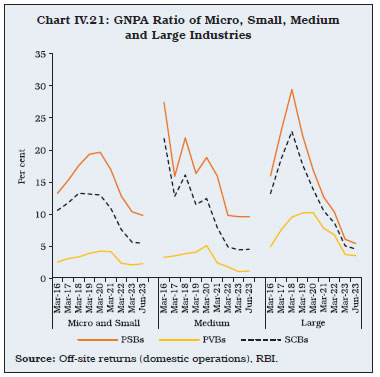

Source: RBI. | IV.38 Based on the date of occurrence of frauds, the average amount involved declined during 2022-23, with the number of cases concentrated in card or internet related frauds (Table IV.15). IV.39 The number of fraud cases reported by PVBs accounted for 66.2 per cent of the total (Chart IV.17a). In terms of amount involved, PSBs had a higher share (Chart IV.17b). While the majority of the frauds in PSBs were related to advances, PVBs accounted for a majority of card/internet and cash-related cases (Chart IV.17c). | Table IV.15: Frauds in Various Banking Operations Based on the Date of Occurrence | | (Amount in ₹ crore) | | Area of Operation | Prior to 2020-21 | 2020-21 | 2021-22 | 2022-23 | 2023-24 (April - Sep) | | Number of frauds | Amount involved | Number of frauds | Amount involved | Number of frauds | Amount involved | Number of frauds | Amount involved | Number of frauds | Amount involved | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | | Advances | 7,530 | 1,69,225 | 1,710 | 10,660 | 1,688 | 6,469 | 1,303 | 1,094 | 199 | 26 | | Off-balance Sheet | 47 | 1,848 | 11 | 109 | 2 | 27 | 3 | 0 | 0 | 0 | | Forex Transactions | 3 | 128 | 4 | 2 | 9 | 8 | 11 | 16 | 2 | 0 | | Card/Internet | 981 | 100 | 2,504 | 134 | 4,230 | 143 | 9,812 | 520 | 7382 | 285 | | Deposits | 533 | 456 | 430 | 569 | 422 | 106 | 551 | 124 | 606 | 34 | | Inter-Branch Accounts | 3 | 0 | 3 | 2 | 1 | 0 | 1 | 0 | 0 | 0 | | Cash | 128 | 27 | 479 | 61 | 931 | 101 | 1011 | 112 | 124 | 19 | | Cheques/DDs, etc. | 98 | 62 | 165 | 164 | 167 | 29 | 88 | 19 | 24 | 7 | | Clearing Accounts, etc. | 13 | 1 | 9 | 3 | 17 | 4 | 10 | 0 | 1 | 0 | | Others | 285 | 138 | 275 | 124 | 192 | 66 | 352 | 261 | 25 | 6 | | Total | 9,621 | 1,71,985 | 5,590 | 11,828 | 7,659 | 6,953 | 13,142 | 2,146 | 8,363 | 377 | Notes: 1. Refers to frauds of ₹1 lakh and above.

2. The figures reported by banks and financial institutions are subject to change based on revisions filed by them.

3. Frauds reported in a year could have occurred several years prior to year of reporting.

Source: RBI. |

4.6 Enforcement Actions IV.40 The increase in instances of penalties imposed on regulated entities (REs) during 2022-23 was led by co-operative banks. For both PSBs and PVBs, they declined during the year. The average penalty per instance was the highest for PVBs (Table IV.16). 5. Sectoral Bank Credit and NPAs IV.41 The acceleration in gross bank credit during 2022-23 was led by personal loans and credit extended to the services sector. Within personal loans, the growth in credit card receivables, which are a form of unsecured lending, rose sharply. Services sector credit was driven by lending to NBFCs (Table IV.17). | Table IV.16: Enforcement Actions | | Regulated Entity | 2021-22 | 2022-23 | | Instances of Imposition of Penalty | Total Penalty

(₹ crore) | Instances of Imposition of Penalty | Total Penalty

(₹ crore) | | 1 | 2 | 3 | 4 | 5 | | Public Sector Banks | 13 | 17.6 | 7 | 3.7 | | Private Sector Banks | 16 | 29.4 | 7 | 12.2 | | Co-operative Banks | 145 | 12.1 | 176 | 14.0 | | Foreign Banks | 4 | 4.3 | 5 | 4.7 | | Payments Banks | - | - | - | - | | Small Finance Banks | 1 | 1.0 | 2 | 1.0 | | Regional Rural Banks | - | - | 1 | 0.4 | | NBFCs | 10 | 1.0 | 11 | 4.4 | | HFCs | - | - | 2 | 0.1 | | Total | 189 | 65.3 | 211 | 40.4 | | Source: RBI. | IV.42 The GNPA ratio remained the highest for the agricultural sector and the lowest for retail loans as at end-September 2023. The asset quality of the industrial sector improved further, with its GNPA ratio at 4.2 per cent at end-September 2023. The variation of asset quality between bank groups has narrowed over the years (Chart IV. 18). IV.43 The improvement in asset quality during 2022-23 was broad-based across industries, with notable gains in mining and quarrying, construction, engineering and basic metals. The gems and jewellery industry has the highest GNPA ratio due to legacy issues (Chart IV.19). 5.1 Credit to the MSME Sector IV.44 Credit to micro and small enterprises had accelerated during 2020-21 and 2021-22, reflecting benefits under the Emergency Credit Line Guarantee Scheme (ECLGS) launched in May 2020. Although the growth rate decelerated subsequently, it remained higher than the credit growth to large industries (Chart IV.20). Within industry, the reduction in the GNPA ratio of large industries from 22.9 per cent at end-March 2018 to 4.6 per cent at end-June 2023 was noteworthy (Chart IV.21). | Table IV.17: Sectoral Deployment of Gross Bank Credit by SCBs | | (Amount in ₹ crore) | | | Outstanding | Per cent variation (y-o-y) | | Mar-2021 | Mar-2022 | Mar-2023 | 2021-22 | 2022-23 | | 1 | | 2 | 3 | 4 | 5 | 6 | | 1 | Agriculture and Allied Activities | 13,29,618 | 14,61,719 | 16,87,191 | 9.9 | 15.4 | | 2 | Industry (Micro and Small, Medium and Large) | 29,34,689 | 31,56,067 | 33,36,722 | 7.5 | 5.7 | | | 2.1 Micro and Small | 4,33,192 | 5,32,179 | 5,98,390 | 22.9 | 12.4 | | | 2.2 Medium | 1,45,209 | 2,25,885 | 2,53,384 | 55.6 | 12.2 | | | 2.3 Large | 23,56,288 | 23,98,004 | 24,84,949 | 1.8 | 3.6 | | 3 | Services, of which | 27,70,713 | 30,11,975 | 36,08,574 | 8.7 | 19.8 | | | 3.1 Computer Software | 19,816 | 20,899 | 21,559 | 5.5 | 3.2 | | | 3.2 Tourism, Hotels and Restaurants | 59,525 | 64,378 | 66,466 | 8.2 | 3.2 | | | 3.3 Trade | 6,28,249 | 6,96,301 | 8,19,921 | 10.8 | 17.8 | | | 3.4 Commercial Real Estate | 2,89,474 | 2,91,168 | 3,14,604 | 0.6 | 8.0 | | | 3.5 Non-Banking Financial Companies (NBFCs)# | 9,48,568 | 10,22,399 | 13,31,097 | 7.8 | 30.2 | | 4 | Personal Loans, of which | 30,09,013 | 33,86,982 | 40,85,168 | 12.6 | 20.6 | | | 4.1 Consumer Durables | 17,265 | 17,088 | 20,044 | -1.0 | 17.3 | | | 4.2 Housing (including Priority Sector Housing) | 14,92,302 | 16,84,424 | 19,36,428 | 12.9 | 15.0 | | | 4.3 Advances against Fixed Deposits (including FCNR (B), NRNR Deposits, etc.) | 77,928 | 83,379 | 1,21,897 | 7.0 | 46.2 | | | 4.4 Advances to Individuals against Share, Bonds, etc. | 5,400 | 6,261 | 6,778 | 15.9 | 8.3 | | | 4.5 Credit Card Outstanding | 1,31,704 | 1,48,416 | 1,94,282 | 12.7 | 30.9 | | | 4.6 Education | 78,131 | 82,723 | 96,847 | 5.9 | 17.1 | | | 4.7 Vehicle Loans | 3,68,412 | 4,00,968 | 5,00,299 | 8.8 | 24.8 | | | 4.8 Loans against Gold Jewellery | 75,049 | 73,960 | 88,428 | -1.5 | 19.6 | | 5 | Non-food Credit | 1,08,88,255 | 1,18,36,304 | 1,36,55,330 | 9.7 | 15.4 | | 6 | Bank Credit | 1,09,49,509 | 1,18,91,314 | 1,36,75,235 | 9.6 | 15.0 | Notes: 1. Bank credit and non-food credit data are based on Section-42 return, which covers all SCBs, while sectoral non-food credit data are based on sector-wise and industry-wise bank credit (SIBC) return, which covers select banks accounting for about 93 per cent of total non-food credit extended by all SCBs.

2. Data are provisional.

3. Data pertains to the last reporting Friday of the month.

4. Credit data are adjusted for past reporting errors by select SCBs from December 2021 onwards.

5. #: NBFCs include HFCs, PFIs, Microfinance Institutions (MFIs), NBFCs engaged in gold loan and others.

Source: RBI. |

IV.45 Reversing the movements over the previous four consecutive years, PSBs’ credit growth to the MSME sector in 2022-23 exceeded that of PVBs. This led to an increase in the former’s share in total MSME credit from 47.5 per cent in 2021-22 to 48.0 per cent in 2022-23. The average amount of loans extended by PVBs was almost double that of PSBs (Table IV.18). 5.2 Priority Sector Credit IV.46 In recent years, PVBs’ overall credit growth was higher than that of PSBs. As a result, PVBs were required to accelerate their priority sector lending to meet regulatory requirements. During 2022-23, total priority sector advances grew by 10.8 per cent, led by PVBs (growth rate of 15.7 per cent). In comparison, the priority sector lending of PSBs grew by 7.1 per cent.

| Table IV.18: Credit Flow to the MSME sector by SCBs | | (Number of accounts in lakh, amount outstanding in ₹ crore) | | Bank Groups | Items | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | | Public Sector Banks | No. of Accounts | 113 | 111 | 151 | 150 | 139 | | | | (1.8) | (-1.9) | (36.1) | (-0.7) | (-7.4) | | | Amount Outstanding | 8,80,033 | 8,93,315 | 9,08,659 | 9,55,860 | 10,84,953 | | | | (1.8) | (1.5) | (1.7) | (5.2) | (13.5) | | Private Sector Banks | No. of Accounts | 205 | 271 | 267 | 113 | 73 | | | | (38.4) | (31.8) | (-1.4) | (-57.7) | (-35.2) | | | Amount Outstanding | 5,63,678 | 6,46,988 | 7,92,042 | 9,69,844 | 10,89,833 | | | | (37.2) | (14.8) | (22.4) | (22.4) | (12.4) | | Foreign Banks | No. of Accounts | 2 | 3 | 3 | 2 | 2 | | | | (9.3) | (14.1) | (-5.1) | (-19.0) | (-26.3) | | | Amount Outstanding | 66,939 | 73,279 | 83,224 | 85,352 | 85,349 | | | | (36.9) | (9.5) | (13.6) | (2.6) | (0.0) | | All SCBs | No. of Accounts | 321 | 384 | 420 | 265 | 213 | | | | (22.6) | (19.8) | (9.4) | (-37.0) | (-19.4) | | | Amount Outstanding | 15,10,651 | 16,13,582 | 17,83,925 | 20,11,057 | 22,60,135 | | | | (14.1) | (6.8) | (10.6) | (12.7) | (12.4) | Note: Figures in the parentheses indicate y-o-y growth rates.

Source: RBI. |

| Table IV.19: Priority Sector Lending by Banks | | (At end-March 2023) | | (Amount in ₹ crore) | | | Target/ sub- target (per cent of ANBC/ CEOBE) | Public Sector Banks | Private Sector Banks | Foreign Banks | Small Finance Banks | Scheduled Commercial Banks | | Amount outstanding | Per cent of ANBC/ CEOBE | Amount outstanding | Per cent of ANBC/ CEOBE | Amount outstanding | Per cent of ANBC/ CEOBE | Amount outstanding | Per cent of ANBC/ CEOBE | Amount outstanding | Per cent of ANBC/ CEOBE | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | | Total Priority Sector Advances | 40/75* | 28,36,168 | 43.7 | 19,51,075 | 45.3 | 2,30,976 | 42.8 | 94,999.3 | 88.2 | 51,13,218 | 44.7 | | of which | | | | | | | | | | | | | Total Agriculture | 18 | 12,77,359 | 19.7 | 7,53,591 | 17.5 | 57,998 | 18.2 | 29,261 | 27.2 | 21,18,210 | 18.9 | | Small and Marginal Farmers | 9.5 | 7,39,768 | 11.4 | 3,64,356 | 8.5 | 35,029 | 11.0 | 20,779 | 19.3 | 11,59,932 | 10.3 | | Non-corporate Individual Farmers# | 13.78 | 9,98,667 | 15.4 | 5,52,916 | 12.8 | 42,228 | 13.2 | 28,437 | 26.4 | 16,22,248 | 14.5 | | Micro Enterprises | 7.5 | 5,03,933 | 7.8 | 3,81,720 | 8.9 | 24,150 | 7.6 | 30,798 | 28.6 | 9,40,601 | 8.4 | | Weaker Sections | 11.5 | 9,33,799 | 14.4 | 4,96,360 | 11.5 | 37,878 | 11.9 | 46,980 | 43.6 | 15,15,016 | 13.5 | Notes: 1. Amount outstanding and achievement percentages are based on the average achievement of banks for all the quarters of the financial year.

2. *: Total priority sector lending target for SFBs is 75 per cent.

3. #: Target for non-corporate farmers is based on the system-wide average of the last three years’ achievement. For FY 2022-23, the applicable system wide average figure is 13.78 per cent.

4. For FBs having less than 20 branches, only the total PSL target of 40 per cent is applicable.

5. Data are provisional.

Source: RBI. | IV.47 All bank groups managed to achieve their overall priority sector lending targets. However, shortfall was found in non-corporate individual farmers sub-category by FBs10, and PVBs fulfilled their target only for micro enterprises (Table IV.19). Growth in the amount outstanding under operative kisan credit cards (KCC) decelerated in 2022-23 to 8.8 per cent. The slowdown was mainly contributed by northern and eastern regions (Appendix Table IV.8). IV.48 Growth in the total trading volume of priority sector lending certificates (PSLCs) decelerated during 2022-23. Except for the general category, the trading volume of PSLCs increased for all segments and was the highest in the small and marginal farmers (SMF) category (Table IV. 20). | Table IV.20: Trading Volume of PSLCs | | (in ₹ crore) | | | PSLC-Agriculture

(PSLC-A) | PSLC-Micro Enterprises

(PSLC-ME) | PSLC-Small and Marginal Farmers

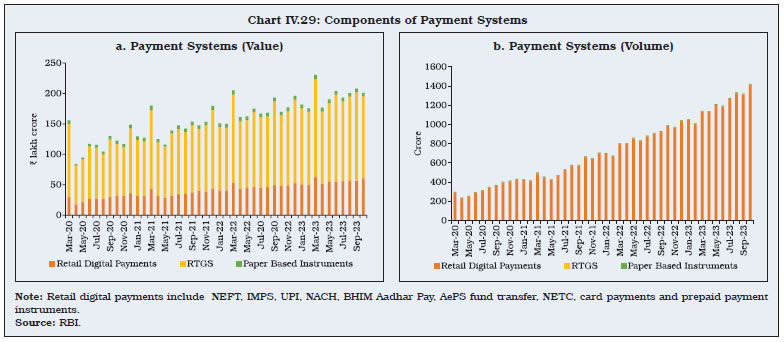

(PSLC-SMF) | PSLC-General

(PSLC-G) | Total | | 1 | 2 | 3 | 4 | 5 | 6 | | 2016-17 | 4,101 | 2,693 | 22,986 | 20,017 | 49,797 | | 2017-18 | 15,936 | 19,100 | 69,622 | 79,672 | 1,84,330 | | 2018-19 | 37,067 | 45,373 | 1,12,505 | 1,32,486 | 3,27,431 | | 2019-20 | 54,102 | 97,623 | 1,45,801 | 1,70,263 | 4,67,789 | | 2020-21 | 60,823 | 1,03,576 | 1,98,231 | 2,26,534 | 5,89,164 | | 2021-22 | 59,274 | 1,04,276 | 2,28,709 | 2,70,131 | 6,62,390 | | 2022-23 | 88,100 | 1,24,777 | 3,21,759 | 1,78,690 | 7,13,326 | | Source: RBI. |

IV.49 In the last four years, PVBs have outpaced PSBs as sellers of PSLCs (Chart IV.22). IV.50 During 2022-23 and H1:2023-24, the weighted average premium (WAP) decreased for all categories of PSLCs, with PSLC-SMF commanding the highest premium (Table IV.21). IV.51 The GNPA ratio related to priority sector lending declined from 7.4 per cent at end-March 2022 to 5.6 per cent by end-March 2023. Nonetheless, the share of the priority sector in total GNPA of SCBs increased from 43.2 per cent at end-March-2022 to 51.2 per cent at end-March 2023 as NPAs in the non-priority sector declined more sharply. NPAs in the priority sector were led by agricultural defaults. IV.52 While PSBs extended 43.7 per cent of their ANBC/CEOBE to the priority sector, this portfolio contributed to 56.2 per cent of their total NPAs. Priority sector comprises of 88.2 per cent of SFBs’ ANBC/CEOBE, but its share in total NPAs has fallen significantly to 43.2 per cent in 2022-23 from 89.9 per cent in the previous year (Table IV.22). 5.3 Credit to Sensitive Sectors IV.53 SCBs’ exposure to sensitive sectors – real estate and capital markets – rose at a faster pace during 2022-23 and accounted for 24.3 per cent of their total loans and advances. Lending to the real estate sector picked up for both PSBs and PVBs (Chart IV.23a). On the other hand, capital market exposure of PSBs decelerated (Chart IV.23b and Appendix Table IV.9). | Table IV.21: Weighted Average Premium on Various Categories of PSLCs | | (Per cent) | | | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2022-23 (Apr-Sep) | 2023-24 (Apr-Sep) | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | | PSLC-A | 1.17 | 1.55 | 1.37 | 0.62 | 0.88 | 0.27 | | PSLC-ME | 0.44 | 0.88 | 0.95 | 0.16 | 0.60 | 0.09 | | PSLC-SMF | 1.58 | 1.74 | 2.01 | 1.68 | 1.97 | 1.93 | | PSLC-G | 0.35 | 0.46 | 0.6 | 0.19 | 0.22 | 0.02 | | Source: RBI. |

| Table IV.22: Sector-wise GNPAs of Banks | | (At end-March) | | (Amount in ₹ crore) | | Bank Group | Priority Sector | Of which | Non-priority Sector | Total NPAs | | Agriculture | Micro and Small Enterprises | Others | | Amount | Per cent | Amount | Per cent | Amount | Per cent | Amount | Per cent | Amount | Per cent | Amount | Per cent | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | | PSBs | | | | | | | | | | | | | | 2022 | 2,43,655 | 48.0 | 1,10,845 | 21.8 | 96,374 | 19.0 | 36,436 | 7.2 | 2,63,973 | 52.0 | 5,07,628 | 100 | | 2023 | 2,25,638 | 56.2 | 1,14,409 | 28.5 | 80,577 | 20.1 | 30,652 | 7.6 | 1,75,666 | 43.8 | 4,01,304 | 100 | | PVBs | | | | | | | | | | | | | | 2022 | 48,588 | 28.7 | 20,863 | 12.3 | 17,799 | 10.5 | 9,926 | 5.9 | 1,20,431 | 71.3 | 1,69,019 | 100 | | 2023 | 42,293 | 36.7 | 19,999 | 17.3 | 14,569 | 12.6 | 7,724 | 6.7 | 73,052 | 63.3 | 1,15,345 | 100 | | FBs | | | | | | | | | | | | | | 2022 | 2,555 | 18.5 | 481 | 3.5 | 1,638 | 11.9 | 436 | 3.2 | 11,231 | 81.5 | 13,786 | 100 | | 2023 | 2,149 | 22.5 | 221 | 2.3 | 1,542 | 16.2 | 386 | 4.0 | 7,395 | 77.5 | 9,544 | 100 | | SFBs | | | | | | | | | | | | | | 2022 | 6,037 | 89.9 | 1,961 | 29.2 | 2,002 | 29.8 | 2,074 | 30.9 | 682 | 10.1 | 6,719 | 100 | | 2023 | 3,832 | 43.2 | 1,549 | 17.5 | 1,065 | 12.0 | 1,217 | 13.7 | 5,038 | 56.8 | 8,869 | 100 | | All SCBs | | | | | | | | | | | | | | 2022 | 3,00,835 | 43.2 | 1,34,151 | 19.2 | 1,17,813 | 16.9 | 48,871 | 7.0 | 3,96,316 | 56.8 | 6,97,151 | 100 | | 2023 | 2,73,911 | 51.2 | 1,36,178 | 25.5 | 97,753 | 18.3 | 39,980 | 7.5 | 2,61,151 | 48.8 | 5,35,062 | 100 | Notes: 1. Per cent: Per cent of total NPAs.

2. Constituent items may not add up to the total due to rounding off.

Source: Off-site returns (domestic operations), RBI. | 5.4 Unsecured Lending IV.54 Unsecured loans − characterised by absence or inadequacy of collateral − present a higher credit risk for banks in the event of defaults. The share of unsecured advances in total credit of SCBs has been increasing since end-March 2015, reaching 25.5 per cent by end-March 2023. More than 50 per cent of loans by FBs are unsecured, while the share is lower at 27.3 per cent and 22.6 per cent for PVBs and PSBs, respectively (Chart IV.24). The Reserve Bank’s November 2023 measures to increase risk weights on select categories of consumer credit exposure need to be seen in this evolving milieu.

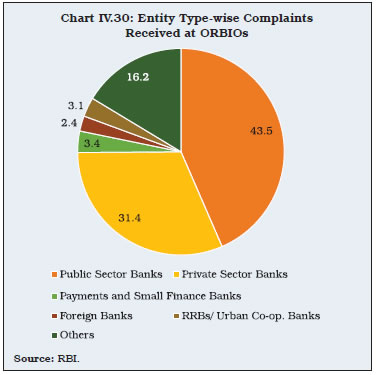

5.5 Borrower Age Profile IV.55 Data sourced from the TransUnion Credit Information Bureau (India) Limited (CIBIL) suggest that 53.1 per cent of retail borrowers were in the 25-45 years age bracket at end-September 2023 (Chart IV.25). 6. Ownership Patterns in Commercial Banks IV.56 The ownership pattern of PVBs underwent a change during 2022-23, with a decline in government ownership particularly in Jammu & Kashmir Bank and an increase in the share of institutional investors such as insurance companies, mutual funds, banks and financial institutions, notably in Karur Vysya Bank and in Yes Bank (Chart IV.26 and Appendix Table IV.10). In the case of PSBs, government ownership remained unchanged at 90.5 per cent of paid-up equity share capital. IV.57 As the asset quality of PSBs has improved, the requirement of capital infusion by the government has declined (Chart IV.27). 7. Corporate Governance IV.58 In the aftermath of the global financial crisis of 2007-09, regulatory reforms in corporate governance have focused on, inter alia, effective board oversight, rigorous risk management, strong internal controls, and compliance. On April 26, 2021 the Reserve Bank issued instructions aimed at achieving robust and transparent risk management and decision-making in banks, thereby promoting public confidence and upholding the safety and soundness of the financial system11. 7.1 Composition of Boards IV.59 Apart from providing checks and balances, independent directors often bring unbiased views, diverse experiences, and expertise to the board and contribute to effective risk management. In the case of PVBs and SFBs, the share of independent directors in the Board and its committees (except for Nomination and Remuneration Committee (NRC) in PVBs) improved in 2022-23 (Table IV.23). IV.60 As per the Reserve Bank’s directions, banks are required to constitute a Risk Management Committee of the Board (RMCB), with a majority of non-executive directors (NED). The chair of the Board may be a member of the RMCB only if he/she has the requisite risk management expertise. The proportion of PVBs where the chair is not a member of the RMCB decreased from 39 per cent at end-March 2022 to 38 per cent at end-March 2023. For SFBs, the proportion decreased from 50 per cent to 42 per cent during the same period. | Table IV.23: Independent Directors on the Board and its Committees | | (At end-March) | | (Share in per cent) | | | Board | RMCB | NRC | Audit Committee of the Board (ACB) | | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | PVBs | 63 | 65 | 65 | 67 | 80 | 78 | 76 | 83 | | SFBs | 68 | 68 | 74 | 76 | 83 | 83 | 83 | 85 | | Source: Annual reports and websites of the banks. | 7.2 Executive Compensation IV.61 Linking the variable component of management compensation to annual performance indicators may inadvertently shift focus to short-term gains at the expense of long-term stability. In order to maintain a balance between such myopia and an incentive-based compensation structure, the Reserve Bank’s revised guidelines require that at least 50 per cent of the total compensation should be variable12. The share of variable pay (VP) in total remuneration (TR) for PVBs increased from 31 per cent at end-March 2021 to 39 per cent at end-March 202213. For SFBs, it increased marginally from 25 per cent to 26 per cent during the same period. At end-March 2022, the share of non-cash component in the VP for PVBs and SFBs decreased to 57 per cent and 34 per cent, from 78 per cent and 41 per cent in the previous year, respectively14. IV.62 The disparity in remuneration between top executives and average employees may induce risk-taking behaviour and can be detrimental to the long-term objectives of the institution. In the context of Indian banks, the gap is the widest in the case of SFBs (Table IV.24). | Table IV.24: Managing Director and Chief Executive Officer’s Remuneration vis-à-vis Average Employee Pay | | (At end-March) | | | PVBs | SFBs | PSBs | | 1 | 2 | 3 | 4 | | 2021 | 25.1 | 58.9 | 2.3 | | 2022 | 26.1 | 58.1 | 2.4 | Note: For each bank, a ratio of their MD & CEO’s remuneration to the average employee pay is calculated. The numbers in the table represent a median of such ratios for the particular bank group.

Source: RBI. | 8. Foreign Banks’ Operations in India and Overseas Operations of Indian Banks IV.63 After a steady rising trend from March 2006 to reach 46 at end-March 2020, the number of FBs in India declined to 44 at end-March 2023. The number of FBs’ branches also declined for the second consecutive year during 2022-23, reflecting rationalisation for cost optimisation (Table IV.25). IV.64 Rationalisation of PSBs’ overseas presence by closing non-viable branches and consolidating operations in the same geography has gathered focus since 2018 to improve cost efficiencies and synergies15. Accordingly, PSBs have shutdown 65 overseas bank branches during the last five years (March 2018 to March 2023). During the same period, PVBs have also reduced their overseas bank branches from 20 to 13 (Chart IV.28 and Appendix Table IV.11). | Table IV.25: Operations of Foreign Banks in India | | | Foreign Banks Operating Through Branches | Foreign Banks Having Representative Offices | | No. of Banks | Branches | | 1 | 2 | 3 | 4 | | Mar-17 | 44 | 295 | 39 | | Mar-18 | 45 | 286 | 40 | | Mar-19 | 45# | 299* | 37 | | Mar-20 | 46# | 308* | 37 | | Mar-21 | 45# | 874* | 36 | | Mar-22 | 45# | 861* | 34 | | Mar-23 | 44# | 782* | 33 | Notes: 1. # Includes two foreign banks namely, SBM Bank (India) Limited and DBS Bank India Limited, which are operating through Wholly Owned Subsidiary (WOS) mode.

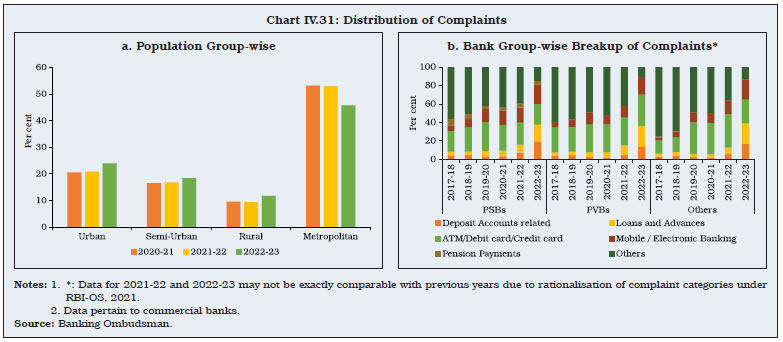

2. *Includes branches of SBM Bank (India) Limited and DBS Bank India Limited (including branches of amalgamated entity, i.e., Lakshmi Vilas Bank as on March 2021) operating through Wholly Owned Subsidiary (WOS) mode.

Source: RBI. |

9. Payment Systems and Scheduled Commercial Banks IV.65 In recent years, India has emerged as a world leader in developing and adopting new technologies in the digital payments landscape. This has been evident not only in terms of growth in digital payments but also in availability of a bouquet of safe, secure, innovative and efficient payment systems. India’s Digital Public Infrastructure (DPI) and its unique open model has been a cornerstone of this transformation. The recognition of the importance of DPI as a priority under India’s G20 presidency at the multilateral forum is expected to further aid its development and deployment. IV.66 In order to enhance the ease of transactions, the upper limit for small value digital payments in offline mode was increased from ₹200 to ₹500 in August 2023. Additionally, ‘Har Payment Digital’ mission was launched during the Digital Payments Awareness Week (DPAW), March 2023 to reinforce the Reserve Bank’s commitment to deepen penetration of digitalisation in the country. 9.1 Digital Payments IV.67 Digital modes of payments are increasingly replacing conventional paper-based instruments such as cheques and demand drafts, with the latter now constituting a negligible share in total payments. In October 2023, 99.6 per cent of total payments in terms of volume and 97.1 per cent in terms of value were made via digital modes (Chart IV.29). IV.68 The growth in volume of total payments decelerated to 57.8 per cent (19.2 per cent in terms of value) during 2022-23 from 63.8 per cent (23.1 per cent in terms of value) during 2021-22 as the post-COVID-19 base effect waned (Table IV.26). Amongst the various options available, the Unified Payments Interface (UPI) has the majority share in volume of transactions, while RTGS, which facilitates high-value transactions on real time basis, accounted for the largest share in terms of value. IV.69 The Reserve Bank launched a composite Digital Payments Index in January 2021 to capture the extent of digitalisation of payments across the country. The index is based on five broad parameters, viz., payment enablers; payment performance; consumer centricity; and demand and supply side factors of payment infrastructure. It is computed semi-annually with March 2018 as the base. At end-March 2023, the index stood at 395.6 as compared to 377.5 at end September 2022, driven by enhanced payment infrastructure and performance.

| Table IV.26: Payment Systems Indicators | | | Volume (Lakh) | Value (₹ crore) | | 2020-21 | 2021-22 | 2022-23 | 2020-21 | 2021-22 | 2022-23 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | | 1. Large Value Credit Transfers – RTGS | 1,592 | 2,078 | 2,426 | 10,55,99,849 | 12,86,57,516 | 14,99,46,286 | | 2. Credit Transfers | 3,17,868 | 5,77,935 | 9,83,621 | 3,35,04,226 | 4,27,28,006 | 5,50,09,620 | | 2.1 AePS (Fund Transfers) | 11 | 10 | 6 | 623 | 575 | 356 | | 2.2 APBS | 14,373 | 12,573 | 17,834 | 1,11,001 | 1,33,345 | 2,47,535 | | 2.3 ECS | - | - | - | - | - | - | | 2.4 IMPS | 32,783 | 46,625 | 56,533 | 29,41,500 | 41,71,037 | 55,85,441 | | 2.5 NACH | 16,465 | 18,758 | 19,257 | 12,16,535 | 12,81,685 | 15,41,815 | | 2.6 NEFT | 30,928 | 40,407 | 52,847 | 2,51,30,910 | 2,87,25,463 | 3,37,19,541 | | 2.7 UPI | 2,23,307 | 4,59,561 | 8,37,144 | 41,03,658 | 84,15,900 | 1,39,14,932 | | 3. Debit Transfers and Direct Debits | 10,457 | 12,189 | 15,343 | 8,65,520 | 10,34,444 | 12,89,611 | | 3.1 BHIM Aadhaar Pay | 161 | 228 | 214 | 2,580 | 6,113 | 6,791 | | 3.2 ECS Dr | - | - | - | - | - | - | | 3.3 NACH | 9,646 | 10,755 | 13,503 | 8,62,027 | 10,26,641 | 12,80,219 | | 3.4 NETC (linked to bank account) | 650 | 1,207 | 1,626 | 913 | 1,689 | 2,601 | | 4. Card Payments | 57,787 | 61,783 | 63,325 | 12,91,799 | 17,01,851 | 21,52,245 | | 4.1 Credit Cards | 17,641 | 22,399 | 29,145 | 6,30,414 | 9,71,638 | 14,32,255 | | 4.2 Debit Cards | 40,146 | 39,384 | 34,179 | 6,61,385 | 7,30,213 | 7,19,989 | | 5. Prepaid Payment Instruments | 49,366 | 65,783 | 74,667 | 1,97,095 | 2,79,416 | 2,87,111 | | 6. Paper-based Instruments | 6,704 | 6,999 | 7,109 | 56,27,108 | 66,50,333 | 71,72,904 | | Total Digital Payments (1+2+3+4+5) | 4,37,068 | 7,19,768 | 11,39,382 | 14,14,58,488 | 17,44,01,233 | 20,86,84,872 | | Total Retail Payments (2+3+4+5+6) | 4,42,180 | 7,24,689 | 11,44,065 | 4,14,85,747 | 5,23,94,049 | 6,59,11,490 | | Total Payments (1+2+3+4+5+6) | 4,43,772 | 7,26,767 | 11,46,491 | 14,70,85,596 | 18,10,51,565 | 21,58,57,776 | | Source: RBI. | 9.2 ATMs IV.70 During 2022-23, the total number of Automated Teller Machines (ATMs) (on-site and off-site) grew by 3.5 per cent, primarily driven by increase in the number of white-label ATMs (WLAs). Amongst the ATMs operated by SCBs at end-March 2023, the share of PSBs and PVBs was 63 per cent and 35 per cent, respectively (Table IV.27 and Appendix Table IV.12). | Table IV.27: Number of ATMs | | (At end-March) | | Sr. No. | Bank Group | On-Site ATMs | Off-site ATMs | Total Number of ATMs | | 2022 | 2023 | 2022 | 2023 | 2022 (3+5) | 2023 (4+6) | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | | I | PSBs | 75,653 | 78,777 | 59,804 | 59,646 | 1,35,457 | 1,38,423 | | II | PVBs | 38,254 | 41,426 | 37,289 | 35,549 | 75,543 | 76,975 | | III | FBs | 701 | 619 | 1,082 | 612 | 1,783 | 1,231 | | IV | SFBs* | 2,185 | 2,797 | 22 | 24 | 2,207 | 2,821 | | V | PBs** | 1 | 1 | 70 | 62 | 71 | 63 | | VI | WLAs | 0 | 0 | 31,499 | 35,791 | 31,499 | 35,791 | | VII | All SCBs (I to V) | 1,16,794 | 1,23,620 | 98,267 | 95,893 | 2,15,061 | 2,19,513 | | VIII | Total (VI+VII) | 1,16,794 | 1,23,620 | 1,29,766 | 1,31,684 | 2,46,560 | 2,55,304 | Notes: 1. *: 11 scheduled SFBs at end-March 2023.

2. **: 4 scheduled PBs at end-March 2023.

Source: RBI. |

| Table IV.28: Geographical Distribution of ATMs: Bank Group Wise@ | | (At end-March 2023) | | Bank group | Rural | Semi - Urban | Urban | Metro-politan | Total | | 1 | 2 | 3 | 4 | 5 | 6 | | Public Sector Banks | 29,293 | 40,334 | 35,218 | 33,578 | 1,38,423 | | | (80.2) | (65.4) | (63.6) | (50.9) | (63.1) | | Private Sector Banks | 6,881 | 20,101 | 18,990 | 31,003 | 76,975 | | | (18.8) | (32.6) | (34.3) | (47) | (35.1) | | Foreign Banks | 109 | 329 | 343 | 450 | 1231 | | | (0.3) | (0.5) | (0.6) | (0.7) | (0.6) | | Small Finance Banks* | 239 | 875 | 837 | 870 | 2,821 | | | (0.7) | (1.4) | (1.5) | (1.3) | (1.3) | | Payments Banks** | 8 | 12 | 26 | 17 | 63 | | | (0.02) | (0.02) | (0.05) | (0.03) | (0.03) | | All SCBs | 36,530 | 61,651 | 55,414 | 65,918 | 2,19,513 | | | (100) | (100) | (100) | (100) | (100) | | All SCBs (y-o-y growth) | 1.39 | 2.30 | 0.39 | -0.47 | 0.82 | | WLAs | 18,346 | 11,583 | 3,813 | 2,049 | 35,791 | | WLAs (y-o-y growth) | 11.8 | 13.2 | 21.0 | 20.2 | 13.6 | Notes: 1. Figures in parentheses indicate percentage share of total ATMs in each geographical region.

2. *: 11 scheduled SFBs at end-March 2023.

3. **: 4 scheduled PBs at end-March 2023.

4. @: Data include ATMs and Cash Recycling Machines (CRMs).

Source: RBI. | IV.71 At end-March 2023, ATMs of PSBs were more evenly distributed across geographies than other bank groups whose ATMs were skewed towards urban and metropolitan areas. In contrast, a majority (51 per cent) of WLAs were concentrated in rural areas (Table IV.28). 10. Consumer Protection IV.72 Consumer education and protection is an integral component of the Reserve Bank’s full-service central banking function. Towards this end, technology is being extensively leveraged to enhance efficiencies in the grievance redressal mechanism. 10.1 Grievance Redressal IV.73 During 2022-23, the number of complaints received under the Reserve Bank - Integrated Ombudsman Scheme (RB-IOS) increased by 68.2 per cent, partly due to simplification of procedures for lodging of complaints. Of the 7,03,544 complaints received against REs, 33.4 per cent were handled by the Office of Reserve Bank of India Ombudsmen (ORBIOs) and the rest were disposed at the Centralised Receipt and Processing Centre (CRPC). The number of complaints against REs dealt at the ORBIOs declined y-o-y by 22.9 per cent in 2022-23 due to structural changes in the Ombudsman framework which led to filtering out of non-maintainable complaints at the level of CRPC and on the Complaint Management Portal. Majority of the complaints received at the ORBIOs during the year pertained to banks (83.8 per cent) (Chart IV.30). IV.74 Under the RB-IOS, effective November 2021, complaint categories were rationalised to make deficiency in service the sole ground for lodging a complaint. Consequently, data on nature of complaints are not strictly comparable across the financial years. During 2022-23, grievances related to loans and advances against banks, NBFCs and other REs accounted for more than one-fourth of the overall complaints received. The share of the top five categories, consisting of complaints received for loans and advances, mobile/ electronic banking, deposit accounts, credit cards and ATM/ debit cards, increased from 54.7 per cent during 2021-22 to 85.8 per cent during 2022-23 (Table IV.29).  IV.75 The share of complaints from urban, semi-urban and rural areas saw an uptick during the year, partly reflecting intensive public awareness programmes conducted across the country (Chart IV.31a). For both PSBs and PVBs, complaints related to ATM/ debit cards/ credit cards constituted the highest share during 2022-23, followed by mobile/ electronic banking related grievances in case of PSBs and complaints concerning loans and advances in case of PVBs (Chart IV.31b and Appendix Table IV.13). 10.2 Deposit Insurance IV.76 Deposit insurance extended by the Deposit Insurance and Credit Guarantee Corporation (DICGC) is an important financial safety net which helps preserve public confidence, especially of small depositors. The scheme covers all commercial banks, including LABs, PBs, SFBs, RRBs and co-operative banks with an insurance cover limit of ₹5 lakh per deposit account. As on March 31, 2023 depositors of 2,026 banks (139 commercial banks and 1,887 co-operative banks) were insured under the scheme (Table IV.30). | Table IV.29: Nature of Complaints at RBIOs | | | 2020-21 | 2021-22# | 2022-23# | | 1 | 2 | 3 | 4 | | Loans and Advances | 20,218 | 30,734 | 59,762 | | Mobile / Electronic Banking | 44,385 | 42,271 | 43,167 | | Deposit Accounts | 8,580 | 16,989 | 34,481 | | Credit Cards | 40,721 | 34,828 | 34,151 | | ATM/ Debit Cards | 60,203 | 41,849 | 29,929 | | Others | 39,686 | 36,607 | 22,551 | | Pension Payments | 4,966 | 6,206 | 4,380 | | Remittances | 3,394 | 3,443 | 2,940 | | Para-Banking | 1,236 | 1,608 | 2,782 | | Notes and Coins | 332 | 302 | 511 | | Non-observance of Fair Practice Code $ | 33,898 | 37,880 | 20 | | Levy of Charges without Prior Notice $ | 20,949 | 14,519 | 3 | | DSAs and Recovery Agents $ | 2,440 | 1,640 | 7 | | Failure to Meet Commitments $ | 35,999 | 22,420 | 5 | | Non-adherence to BCSBI Codes $ | 14,490 | 5,069 | 1 | | Out of Purview of BO Scheme $ | 10,250 | 8,131 | - | | Total | 3,41,747 | 3,04,496* | 2,34,690^ | Notes: 1. # : Data pertain to commercial banks, NBFCs and other REs.

2. * : Excludes 1,13,688 complaints handled at CRPC.

3. ^ : Excludes 4,68,854 complaints handled at CRPC.

4. $ : Decline is due to recategorisation of complaints and structural changes in the Ombudsman framework under RB-IOS, 2021.

Source: RBI. |

| Table IV.30: Bank Group-wise Insured Deposits | | (At end-March 2023) | | (Amount in ₹ crore) | | Bank Groups | No. of Insured Banks | Insured Deposits (ID) | Assessable Deposits (AD)* | ID / AD (per cent) | | 1 | 2 | 3 | 4 | 5 | | I. Commercial Banks | 139 | 79,22,120 | 1,83,48,838 | 43.2 | | i) Public Sector Banks | 12 | 52,20,324 | 1,05,07,639 | 49.7 | | ii) Private Sector Banks | 21 | 21,20,937 | 62,37,833 | 34.0 | | iii) Foreign Banks | 43 | 50,037 | 8,62,909 | 5.8 | | iv) Small Finance Banks | 12 | 66,745 | 1,63,183 | 40.9 | | v) Payments Banks | 6 | 12,533 | 12,694 | 98.7 | | vi) Regional Rural Banks | 43 | 4,50,675 | 5,63,377 | 80.0 | | vii) Local Area Banks | 2 | 869 | 1,204 | 72.2 | | II. Co-operative Banks | 1,887 | 7,09,139 | 11,10,076 | 63.9 | | i) Urban Co-operative Banks | 1,502 | 3,62,991 | 5,34,413 | 67.9 | | ii) State Co-operative Banks | 33 | 64,041 | 1,46,931 | 43.6 | | iii) District Central Co-operative Banks | 352 | 2,82,107 | 4,28,733 | 65.8 | | Total | 2,026 | 86,31,259 | 1,94,58,915 | 44.4 | Note: *: Assessable deposits mean overall deposits, including portions which are not provided insurance cover. Inter-bank deposits and government deposits are excluded from the total deposits to get assessable deposits.